Are the costs of Brexit big or small?

Critics say my estimate – that the British economy is around 5 per cent smaller due to Brexit – is implausibly large. This insight tests their scepticism against other ways to estimate the cost of Brexit.

In a debate I participated in last month, panellists were asked to say how much Brexit had curbed Britain’s economic output. Graham Gudgin of Policy Exchange and Cambridge University’s Centre for Business Research said he thought the costs had been negligible. Julian Jessop of the Institute of Economic Affairs said GDP was around 1 per cent smaller than it would have been, adding that the short-term impact was always going be negative, before the benefits of bespoke regulation and reduced trade barriers with the rest of the world kicked in. Jonathan Portes of UK in a Changing Europe and King’s College London said the costs amounted to around 2.5 per cent of lost GDP.

All their estimates were lower than mine – my model finds that Brexit had reduced the size of the economy by 5.5 per cent in the second quarter of 2022, and all three panellists expressed doubts about my estimate. Graham rejected it outright, saying I should withdraw it, while Jonathan agreed that the ‘synthetic control method’ (also known as the doppelgänger method) is the one most economists would use, but he thought 5 per cent was on the higher end of plausibility. This piece sets out some checks that I have done in response to their scepticism, and why I continue to think the costs of Brexit are larger than they do.

Why does this matter? After all, both Labour and the Conservatives have said that Britain will not rejoin the single market and customs union, let alone the EU. However, identifying the scale of the impact of Brexit is important, because if the costs are small, there is less urgency to make big changes to Britain’s economic model. The Covid pandemic is under control, energy prices are falling, and once inflation has been tamed living standards will start to improve. If, however, the impact of Brexit is large – as my model estimates – then major reforms will be needed to offset the productivity that has been lost.

As a reminder, my model uses an algorithm to identify a ‘doppelgänger’ UK that never left the EU. From a group of 22 advanced economies, the algorithm selects those whose economic performance was most similar to Britain’s between 2009 and 2016 and puts them together to form the doppelgänger. The countries that the algorithm selects to form this synthesised British economy are the US (30 per cent), Germany (15 per cent), New Zealand (14 per cent), Norway (8 per cent), Australia (5 per cent) with other countries making up smaller shares. We can then use the gap between the doppelgänger and the UK, to estimate the size of the loss to GDP after the referendum. That gap was around 5 per cent by December 2021, before the worst of the energy crisis struck (energy prices started to rise precipitously from July 2022) and before Liz Truss and Kwasi Kwarteng’s ill-fated September budget.

It is healthy for my model to be criticised: we can only estimate how much Brexit has hurt the economy by trying to find the best counterfactual we can. The synthetic control method I (and others) have used is well established in the social science literature as a way to estimate counterfactuals. And, as we will see below, it is the worst way to assess Brexit, apart from all the others. Let us consider the alternatives first.

Model check 1: Extrapolating from Britain’s past

The only way we can estimate ‘what would have been’ is to use some sort of counterfactual. One possible method is to use observations from the past. Economic output tends to grow on average at a certain rate per year, unless that rate is interrupted by a prolonged recession. We can use this average rate – ‘trend growth’ – to see how whether the UK deviated from trend after the referendum in 2016.

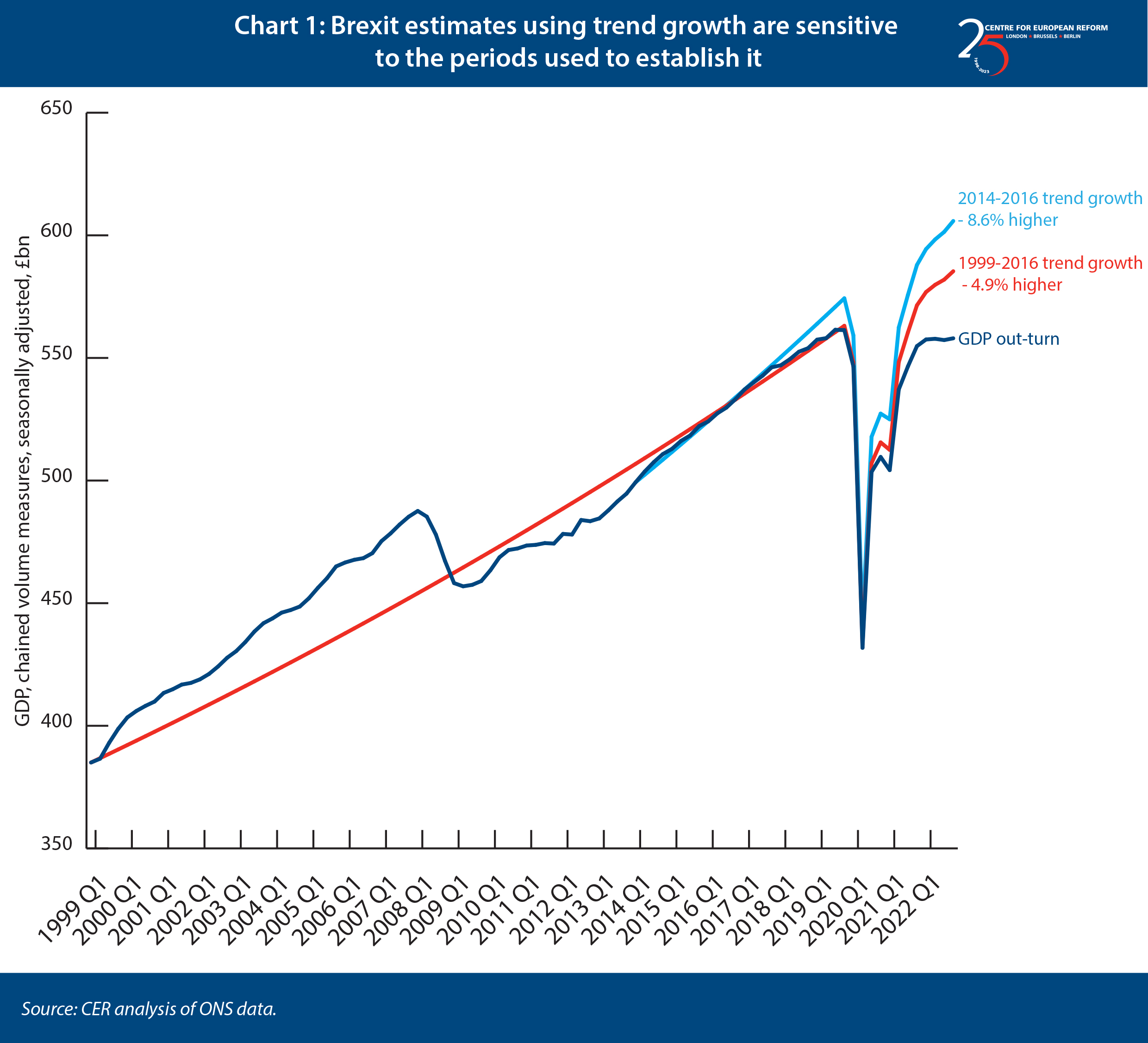

Estimating Brexit costs this way is cruder than the doppelgänger method, because the result is very sensitive to the period used to establish trend growth. Chart 1 adopts the method that Josh Martin and Jonathan Haskel of the Bank of England use to estimate the loss of investment, but substitutes GDP for investment. They take the trend from 1999 to 2016, and then add that quarterly trend growth to each quarter after the Covid nadir in the second quarter of 2020.

The chart shows how this isn’t a very good counterfactual for GDP (this is not a criticism of Martin and Haskel – it’s a fairer way to approach investment, as they discuss here). The recession of 2008-9 drags down the average growth rate, so it is slower than the two periods of expansion between 1999 and 2009 and 2012 to 2020. That means it shows no material impact of Brexit between 2016 and Q1 2021. That seems implausible given the big drop in the value of sterling on the day after the referendum (which raised import prices and slowed consumption growth) and falling net migration from the EU between 2017 and 2019 (which slowed employment growth).

However, if the 2014-16 trend is used, then we end up with an implausible Brexit hit of around 8.6 per cent. That is largely because their method assumes a return to the pre-Covid trend rate of growth, which few other advanced economies have managed.

The doppelgänger method, on the other hand, takes advantage of the fact that rich countries’ economic cycles tend to be somewhat synchronised. Instead of using historical trend growth, we can compare the UK to its peer economies, which are being buffeted by similar shocks (such as global financial conditions and Covid). This means that we have a better counterfactual – one that is experiencing contemporary economic pressures, rather than ones that have determined past rates of growth.

Model check 2: The ranking method

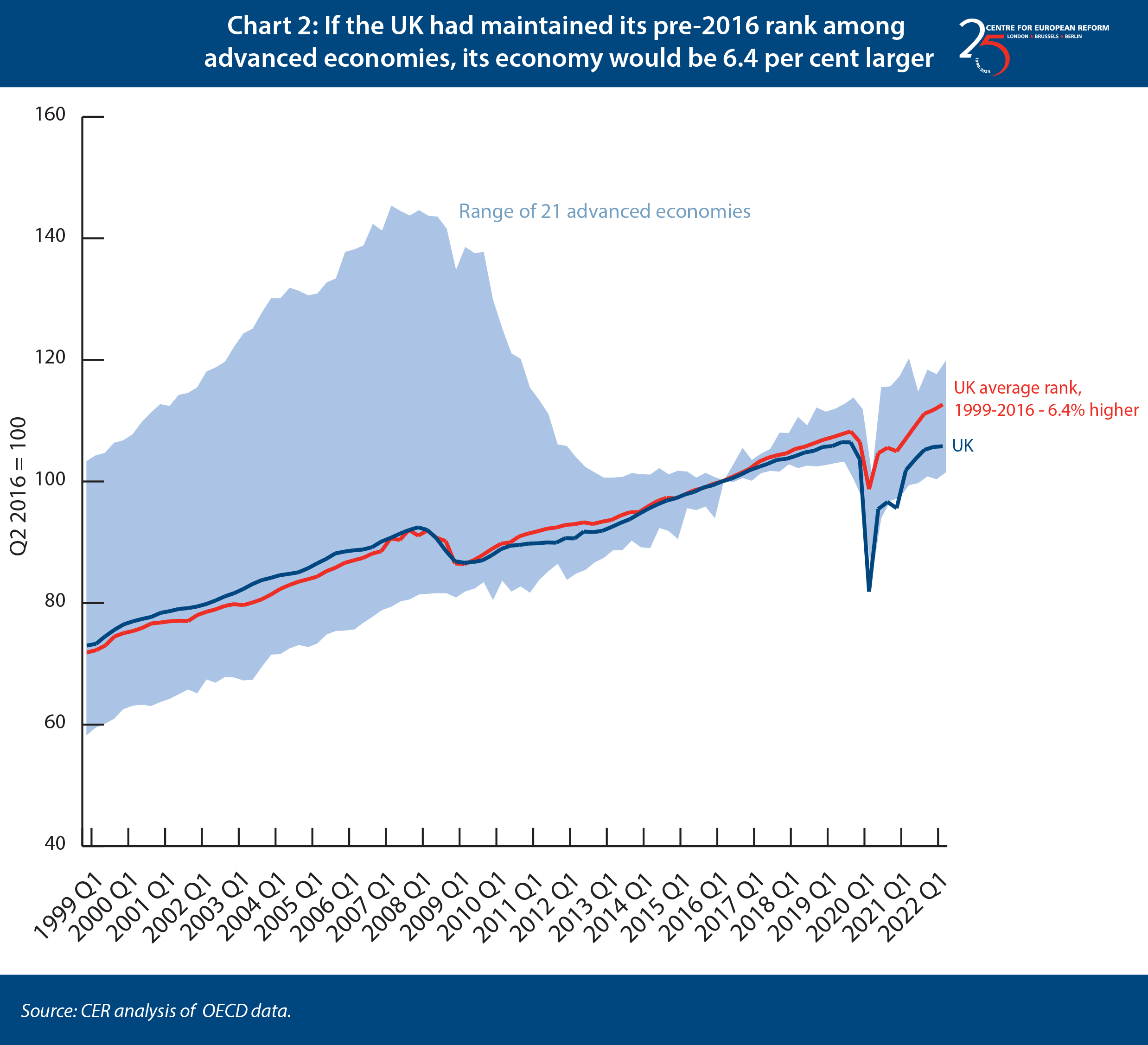

A simple and transparent way to compare the UK to its peer economies is to rank its pre-referendum growth rate against other rich countries. Chart 2 shows the range of 21 economies that the IMF described as advanced in 1995: it’s important to use the most mature economies because developing ones tend to grow faster. (Ireland does not appear because its GDP figures are problematic: many US multinationals book worldwide profits in the country, taking advantage of low corporate tax rates, which means Ireland’s measured output is highly volatile.) The UK was one of the faster growing economies between 1999 and 2016. After 2016, however, growth began to slow compared to the range of other countries.

We can make an estimate using this range. On average, between 1999 and 2016, Britain ranked ninth fastest out of the countries (8.69th to be precise). If Britain had kept its rank after the referendum, by the second quarter of 2022 the UK, its economy would have been 6.4 per cent larger (Chart 2).

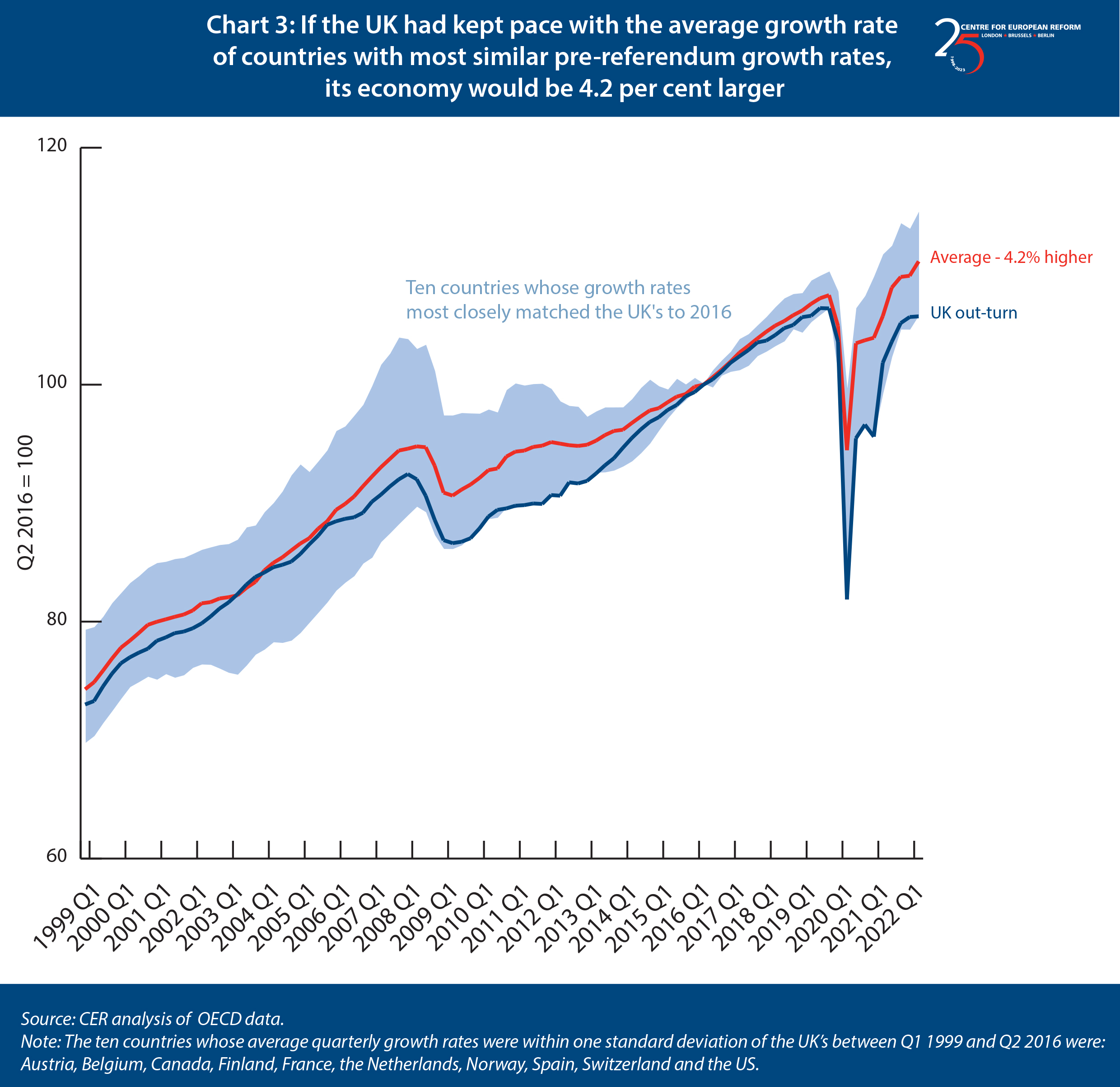

One might object – with good reason – that it would be better to narrow the range of countries to those whose growth rates were most similar to the UK’s up to the referendum. After all, the range of advanced economies in the chart above includes Greece, which struggled through a depression from 2010, with GDP falling by a quarter. Chart 3 plots the UK against a range of ten countries whose growth rates were most similar to that of the UK between Q1 1999 and Q2 2016 (within one standard deviation). If the UK had kept pace with their average pre-referendum growth, by the second quarter of 2022, its economy would have been 4.2 per cent larger (Chart 3).

Model check 3: Comparing the doppelgänger to forecasts

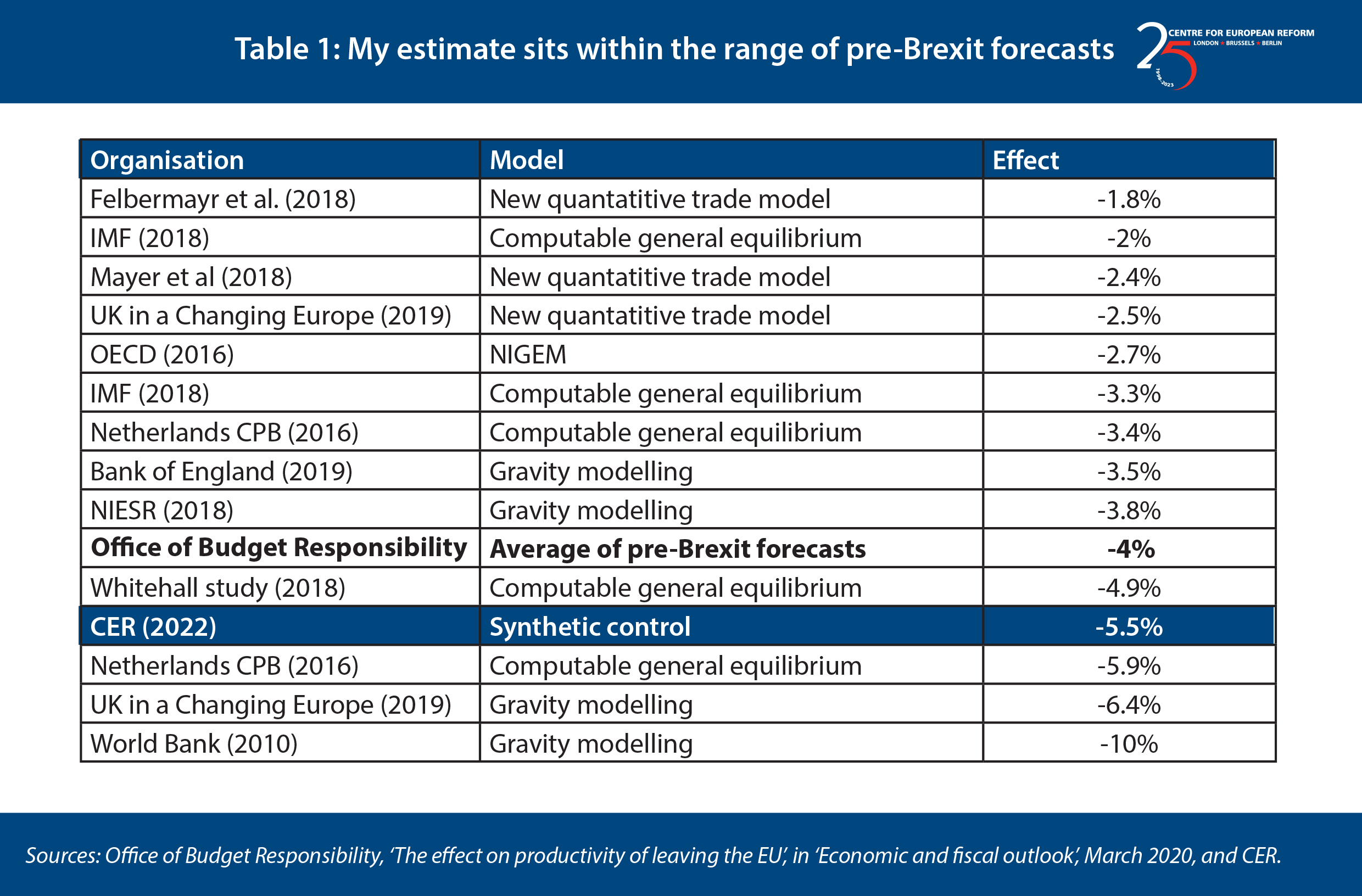

Another way to check the method is to compare its output to forecasts made before the UK left the EU, in which estimates of the Brexit hit to trade, investment and productivity were fed through pre-existing models of the UK economy. The Office of Budget Responsibility took the average of a range of models to arrive at its forecast – that Brexit would reduce productivity by 4 per cent. My estimate is for GDP, whereas productivity is more closely related to GDP per capita, but it provides a sense check of whether my estimate is plausible. As the table shows, my estimate is towards the upper end of the forecasts. But there was a large range: we could only have weak confidence about how big the effects of Brexit would be before the event, because it depended on the model and assumptions that were used.

When making these long-term forecasts, the authors usually said that the full effects would be established after 10 or 15 years. But it is just a convention that the ‘long run’ is about a decade in this case – the models did not specify how long it would take for the costs to show up, and they may have come through more quickly.

Model check 4: What about Covid?

In last month’s debate, one counterargument was I was too willing to blame the UK’s poor economic performance on Brexit, rather than Covid. It was fair to hone in on the Covid problem: this is the biggest source of uncertainty. The method’s estimates will become less reliable over time, because it focuses on the relationships between different economies between 2009 and 2016. Changes thereafter might have nothing to do with Brexit. Covid was a big economic shock, and Britain’s economy might have bounced back more weakly than its peers, perhaps because its economy was particularly damaged by the pandemic, or its relatively underfunded/badly managed health service – take your pick – struggled to cope, leaving more sick people unable to work.

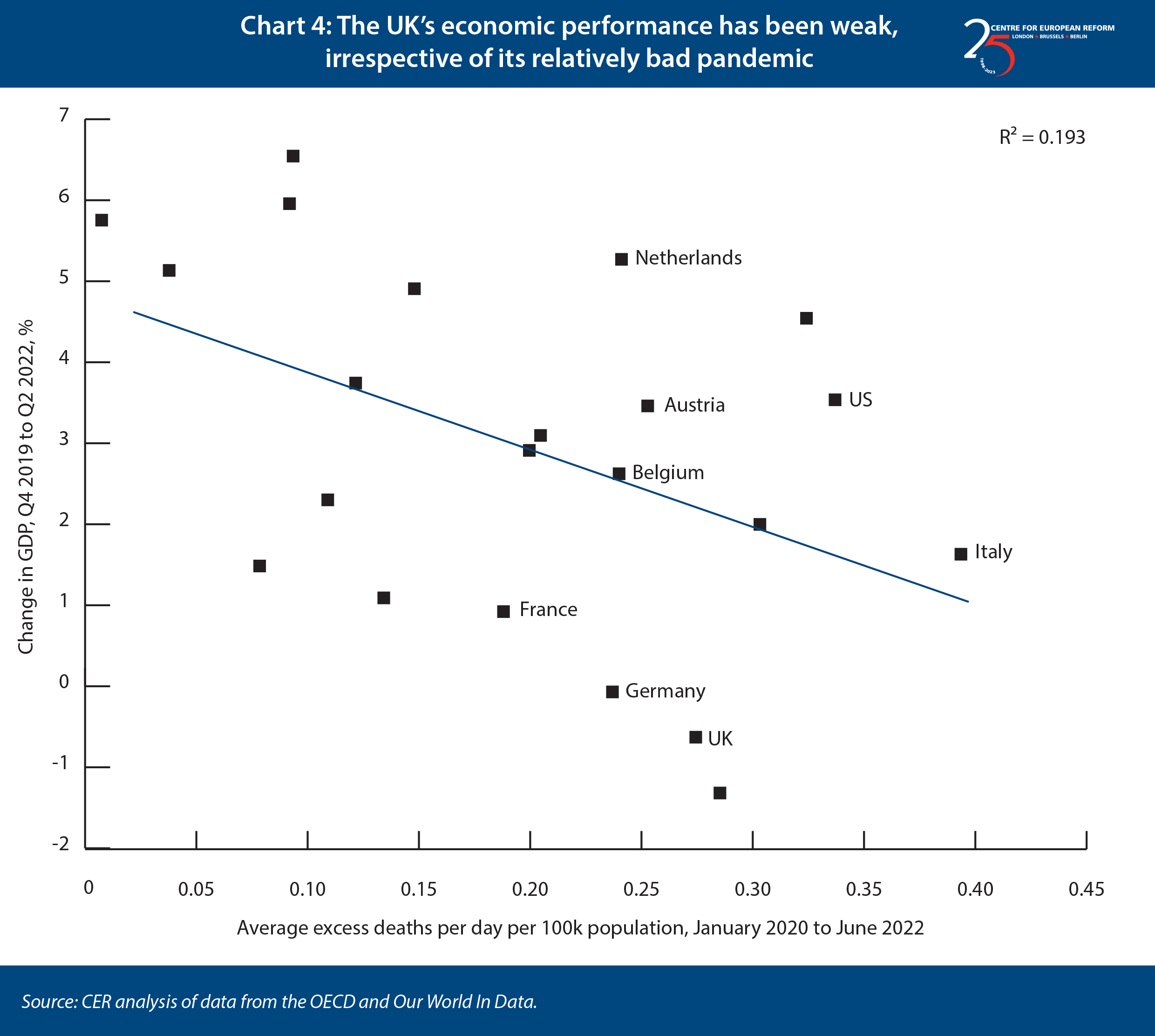

The UK left the single market and customs union when the transition period ended in the middle of the pandemic, but it is difficult to know precisely how much of the UK’s weakness is down to Covid. However, there are two reasons to believe that it’s largely Brexit. First, there is a negative relationship between countries’ Covid death rates and their subsequent economic performance, but it is a very weak one. Chart 4 shows that Italy and the US had higher excess death rates than the UK but a stronger economic recovery. And the UK economy did much worse than its pandemic performance predicted, by a crude comparison to other economies – its growth was far lower than the blue line of best fit.

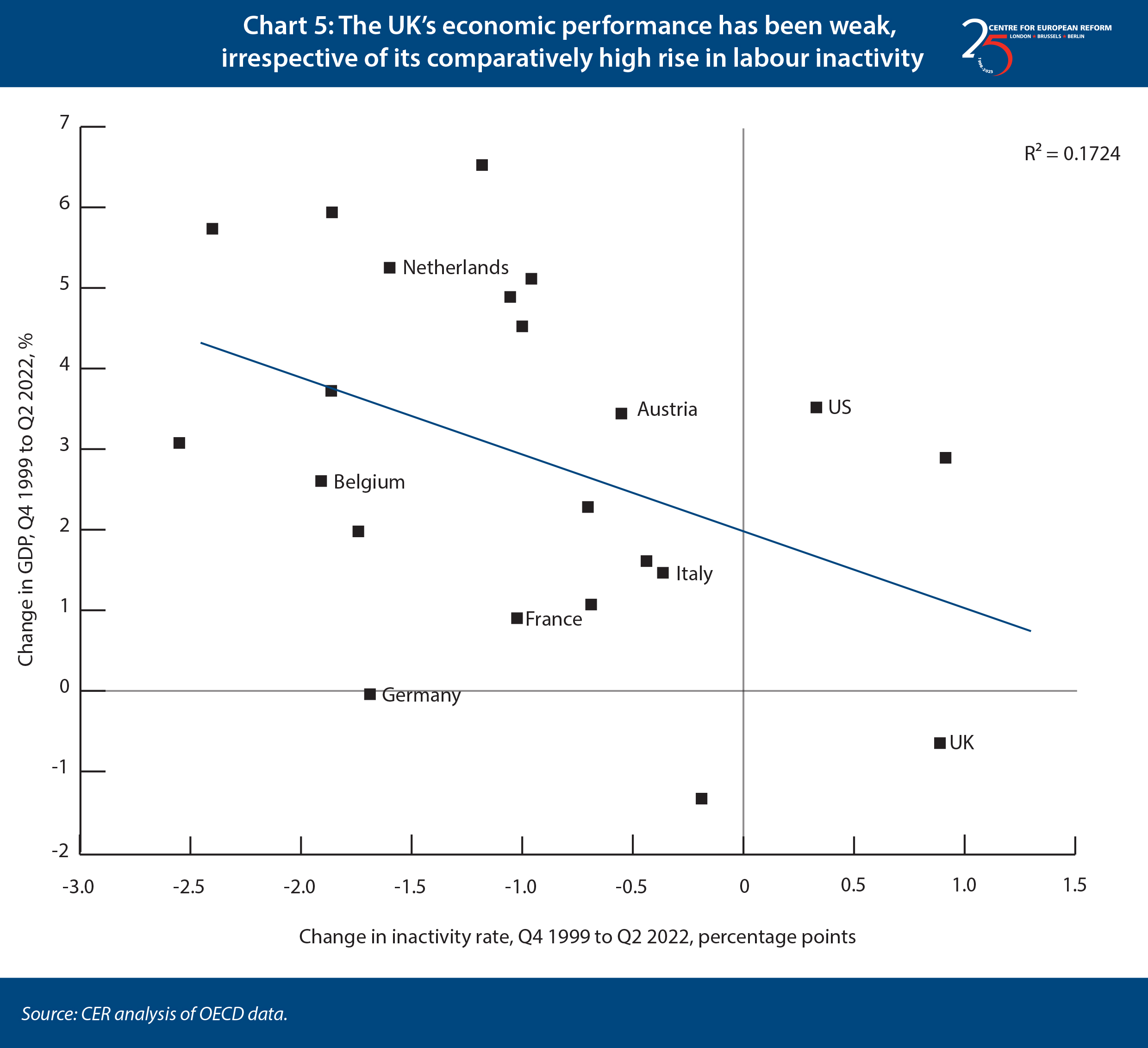

What about the possibility that the UK’s weak performance is due to high rates of sickness, stemming from an overwhelmed NHS? Britain’s growth has been disappointing, and the number of working people who are out of work and not looking for a job – perhaps because of illness, early retirement, raising children or studying – has risen, unlike most other advanced economies. And there is a negative relationship between the change in the inactive population and GDP growth over the course of the pandemic (Chart 5). But again, the relationship is weak, and the UK’s economic performance was particularly poor.

The checks above have some utility, but their weaknesses highlight the benefits of the doppelgänger method. These are:

- Using other countries to compare the UK’s post-referendum performance is better than using the UK’s prior performance, because it’s important to factor in common contemporary shocks, like Covid or falling energy prices in 2015-16.

- It’s important to choose economies that are most similar to the UK – not poorer, faster growing countries like China or countries that suffered from depressions, like Greece.

My version of the method selects countries whose GDP performance was most like that of the UK between 2009 and 2016 to put together a synthesised British economy that did not vote for Leave. But it goes further, by finding those economies whose inflation rates, industrial production-GDP ratios, trade-GDP ratios, average years of schooling of the adult population, and growth of GDP per capita were also most similar to the UK. That means my model produces a counterfactual that is most likely to respond to global shocks, including Covid, in a similar way to the UK.

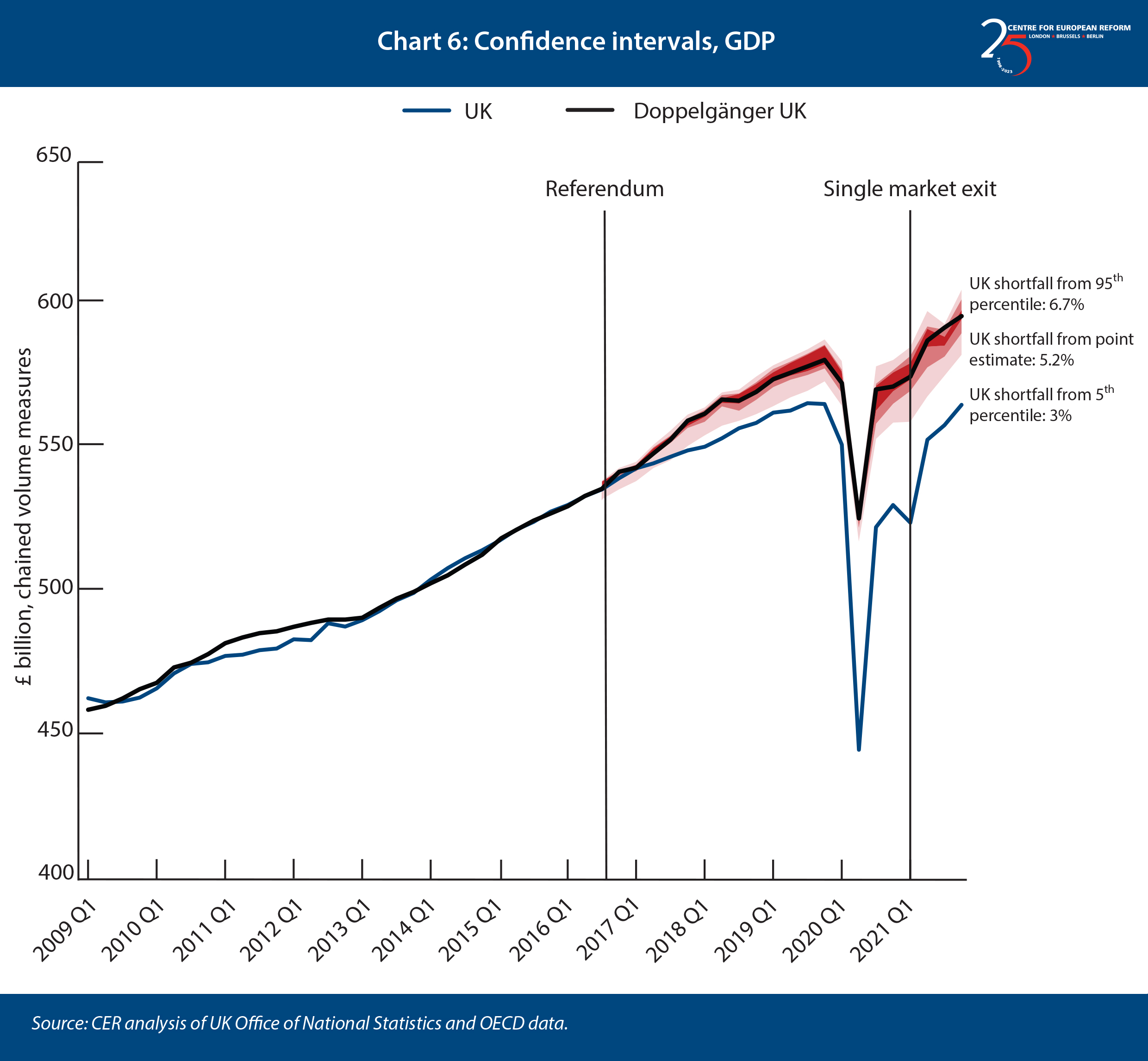

It is possible to assess how confident we can be in the doppelgänger – and its estimate that the UK is around 5 per cent smaller as a result of Brexit – by testing various calibrations. In my last-but-one estimate, I randomly dropped countries from the range that the algorithm could select to try to match UK economic performance, and repeatedly ran the model to get a range of estimates. Around half the time, the US – or any other country from the 22 advanced economies that were included in the range above – was dropped from the model. The results are shown in Chart 6. Crudely, out of 100 estimates, the 5th lowest suggested that the UK economy was 3 per cent smaller as a result of Brexit, and the 95th highest was that it was 6.7 per cent smaller.

If the UK’s poor performance is partly down to Covid, that should be picked up by this check. The UK economy could have been relatively badly hit by Covid, in which case it might be closer to the bottom of the range of potential estimates. But the 5th percentile estimate is still a 3 per cent shortfall – a sizeable impact, and one that is larger than those of my fellow panellists.

It is difficult to be precise, but the doppelgänger method remains the best way to estimate the cost of Brexit when compared to other methods. It should be our central estimate until a better way to identify the counterfactual is found. The evidence points to a big shortfall in GDP as a result of Brexit, and it is important to try to raise growth and not wait for the economy to pick up. I will not be withdrawing the model: Brexit has blown a sizeable hole in Britain’s economic model, and major reforms are needed to recover lost ground.

John Springford is deputy director of the Centre for European Reform.

Related content

The cost of Brexit to June 2022

What can we know about the cost of Brexit so far?

The cost of Brexit: December 2021

Add new comment