Keeping up appearances: What now for UK services trade?

- The UK is a services superpower. But foreign-owned businesses are responsible for 56 per cent of its annual services exports (excluding financial, insurance and transport services).

- However, the UK’s decision to leave the EU’s single market jeopardises its position as a hub for multinational services firms to sell to clients across Europe. Policy-makers in London should take steps to ensure that the slow trickle of business moving to the EU does not become a flood.

- A more mature political discussion about the opportunities available for Britain’s traded services sector is needed. Foreign regulators are reluctant to allow risky services activity to take place outside their jurisdiction, which means there are few opportunities for new cross-border sales. Removing barriers to trade in foreign markets will remain difficult, requiring long-term diplomatic efforts to build trust and understanding.

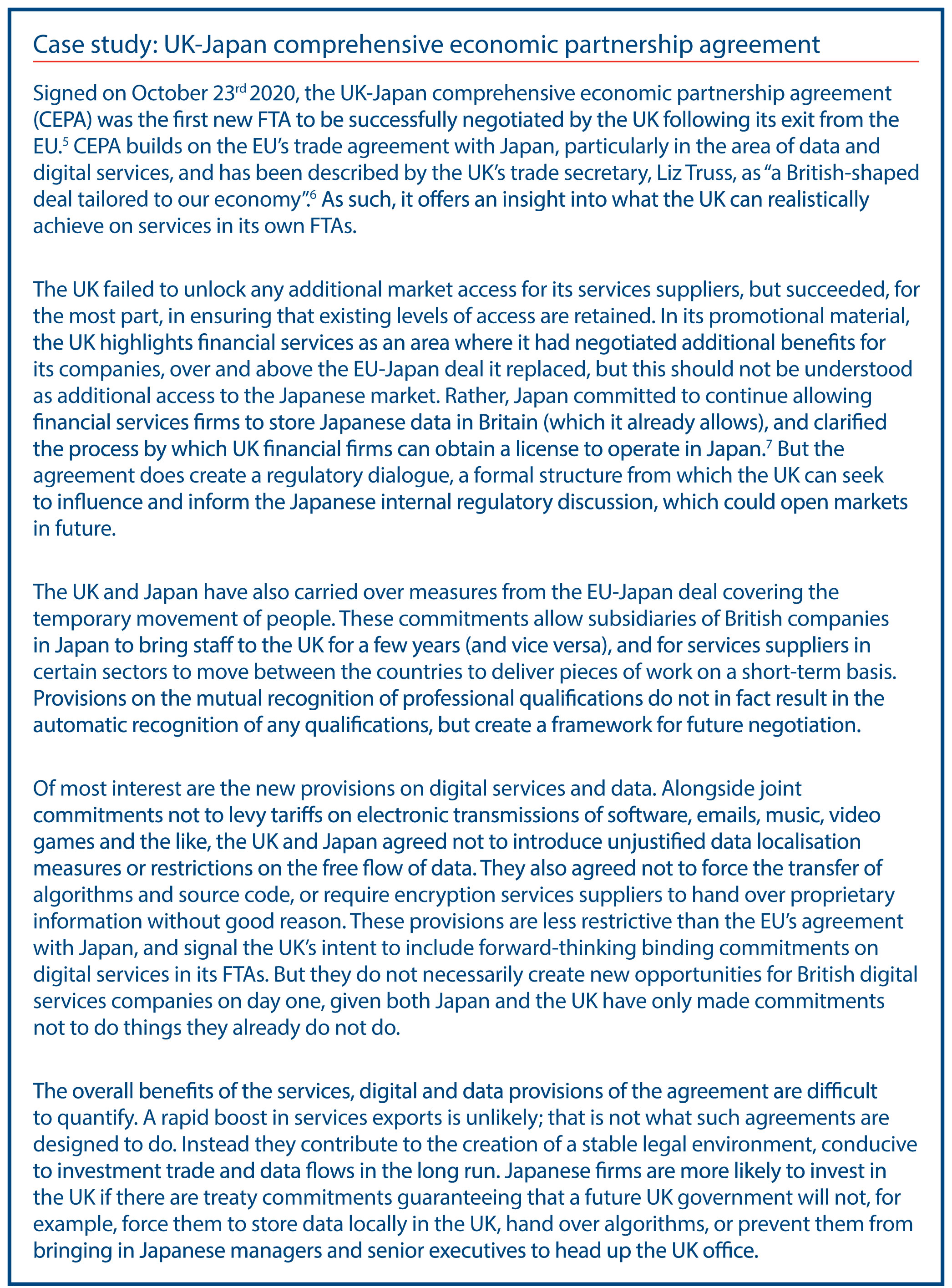

- Free trade agreements (FTAs) have only a small role to play. They are unlikely to provide new market access for UK services exporters – as evidenced by the UK’s recent deal with Japan, which did not unlock any additional Japanese services liberalisation over and above what Japan unilaterally already offers other countries. But trade agreements do prevent partners from rolling back existing levels of openness to British services firms. They can therefore help to ensure a stable policy environment for investors in both directions.

- The UK government should make a priority of creating and maintaining a stable and open policy environment so as to attract investment and people. The UK should avoid the temptation to make a show of diverging from inherited EU rules, so as to avoid further unnecessary regulatory instability. It should also re-engage with the EU on discussions about enhanced labour mobility, to ensure that services workers can move more easily between the UK and the Union.

- As well as doing its best to retain services access to EU markets, the UK should also prioritise scrapping (or drastically reducing) visa application fees for all foreign workers, embedding provisions on the free flow of data in both the UK’s bilateral and multilateral arrangements, and engaging in longer-term formal and informal regulatory dialogue with regulators and politicians to improve access in target markets.

Trade in services is not well understood. Unlike trade in goods, where buyers and sellers physically transport objects across borders, it is possible to sell a service to a client on the other side of the world, unbeknownst to anyone else, without ever leaving the comfort of your living room. The ‘product’ is often intangible – for example advice or analysis – and capturing accurate data on the true value of services being traded across borders has eluded statistical agencies. There are also classification problems: the profits repatriated from the foreign branch of a bank do not register in a country’s national accounts as a services export, yet they are at least in part the result of a foreign country allowing outside financial services providers to operate in their territory.

When it comes to removing barriers to trade in services, there are no tariffs to remove. The rules governing services trade instead focus on whether:

- a person or the software selling services needs to be in the same territory as the person buying the services;

- foreign providers are allowed to sell their services directly to a country’s consumers at all;

- there are restrictions on foreign services suppliers opening local subsidiaries, branches or offices;

- foreign nationals are allowed to provide services in person on a temporary basis;

- qualifications or licenses granted by foreign bodies are recognised or not; and

- there are any numeric restrictions on the quantity or value of a service sold by a foreign provider.

Incomplete data and outdated assumptions about how trade works in the modern world have led policy-makers to both overemphasise and misunderstand the trade policy instruments available to them. Data on cross-border flows in services is patchy and often tells us more about a country’s approach to taxation than its trade policy or the economic impact of trade agreements.1 It is better to think about services trade in terms of investment: where do companies locate the bulk of their operations with the accompanying jobs and value creation when selling into a particular market, and why?

For the past three decades, the UK has been a magnet for international banks and services firms seeking a foothold in the European market. Now that the UK has left the EU’s single market, regulated services providers will find it notably more difficult to sell directly into the EU from Britain. Over time, this friction will lead to capital, workers and output leaving, and investment that would have otherwise come to the UK going elsewhere. Outside the EU, there are few opportunities for UK services providers that have not yet been explored. And the preferred tool of policy-makers, FTAs, will only play a small part in the future international activity of British services firms. Regulators in most countries are reluctant to allow economic activity that they think may pose a systemic risk, like financial services, or a direct risk to consumers, like medical advice, to take place outside their jurisdiction.

The UK should concentrate its efforts on investment, both outwards and inwards, and on shoring up its position as an attractive location for services firms to base themselves. In practice this involves the UK:

- creating a stable policy environment, both unilaterally and via binding treaty commitments;

- retaining access to a large pool of skilled workers via liberalisation of its immigration regime;

- ensuring continued preferential access to the EU market, where possible;

- trying to reduce the risk of restrictions on the cross-border flow of data; and

- engaging in targeted regulatory diplomacy to unlock new opportunities for British companies abroad.

A services trade superpower

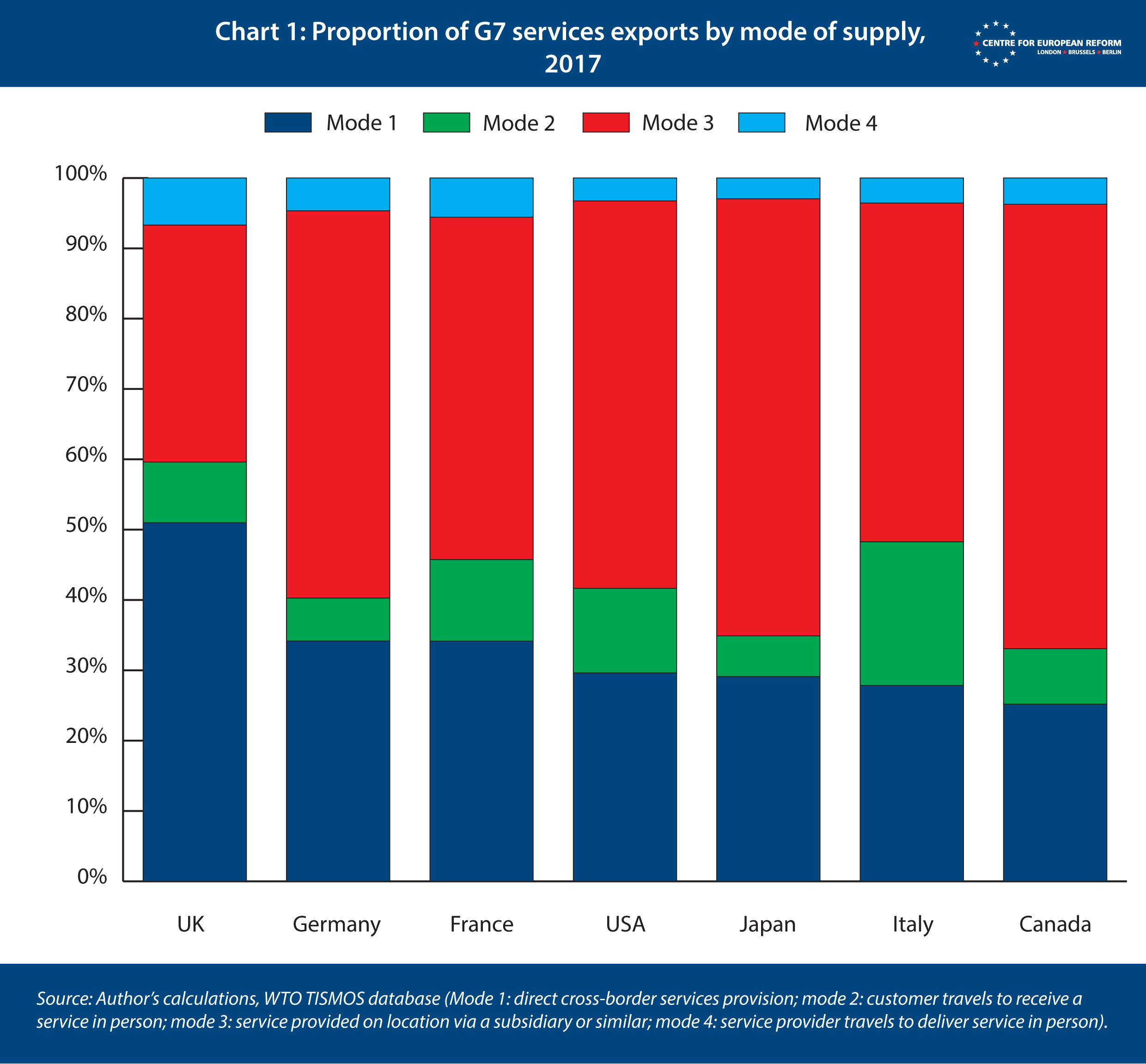

Globally, if a company wants to sell services in a foreign market, more often than not it does so from offices or subsidiaries (mode 3) located in the destination market.2 However, in this respect, the UK is an anomaly. It is the only G7 economy that sees more than 50 per cent of its services directly exported (mode 1) – for example a UK-based architect emailing paid-for designs to a Brazilian property developer – from UK soil to the rest of the world (see Chart 1). With the caveat that the data is far from precise, and inevitably fails to account for all transactions, these numbers show that the UK is a services trade superpower, and suggest that UK services firms are already making good use of existing opportunities to sell directly across borders.

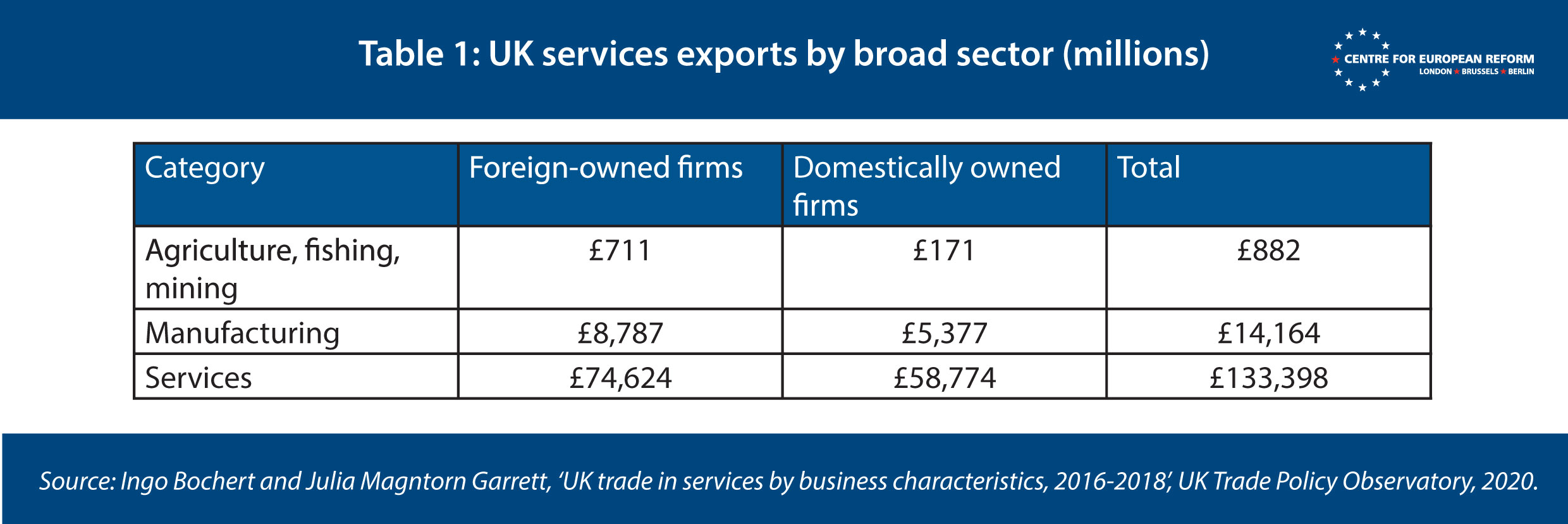

Foreign-owned companies are responsible for most of the UK’s cross-border services sales, particularly to the EU. Drawing on experimental ONS statistics (which exclude financial, insurance and transport services), Ingo Bochert and Julia Magntorn Garrett of the UK Trade Policy Observatory show that foreign-owned businesses export around £85 billion of cross-border services annually from the UK, 56 per cent of the total in the covered sectors (see Table 1).3

However, the UK has decided to leave the EU’s single market, and instead trade with the bloc under the terms of an FTA which removes tariffs and quotas on goods, but does little to facilitate trade in services. The new arrangement means that it will now be more difficult for tightly regulated services suppliers, such as financial, audit, legal and engineering companies, to sell directly to EU-based customers from the UK’s territory.

New restrictions on cross-border sales will lead to a shift in capital away from the UK over time. Future investment in EU-focused activity that would have otherwise been captured by the UK will instead go to the EU. The magnitude of such a shift is difficult to predict – but the largest impact will most likely be felt by the financial, insurance and pensions sectors. The legal, professional, accountancy and transport services sectors will have to adjust as well, but to a lesser extent.4

Britain’s decision to extricate itself from the EU’s regulatory regime jeopardises its position as a European hub. Unless the UK rapidly changes its mind about EU regulation and the free movement of people, there is little it can do to keep hold of activity that, under EU rules, must take place in the single market. However, the UK must also make sure that it remains attractive as a hub for unregulated and global services.

What role is there for new free trade agreements?

British politicians like to emphasise the opportunities that an independent trade policy offers to British services exporters. But the focus on unlocking new export opportunities points to a fundamental misunderstanding of what services provisions in FTAs are for, and what their limitations are.

Ultimately, the openness of a country to foreign services providers rests on the risk tolerance of domestic politicians and regulators.

When a physical product crosses a border, it is possible for a country’s enforcement agencies to intervene directly to make sure the product meets all the relevant criteria necessary to be sold on their market. For services, it is not so simple – especially when the service is delivered via email, telephone or videoconference from a foreign jurisdiction. Domestic policy-makers have to take a decision whether to trust that the rules governing the foreign services provider are equivalent to their own, and whether to trust that foreign authorities will hold the provider to account if something goes wrong. (As with goods trade, governments might also impose restrictions for protectionist reasons, at the behest of local industry.)

In practice, lawmakers are largely unconcerned about services being provided to their citizens from outside their regulatory purview, so long as the services provided pose little threat to consumers or economic stability. For example, the UK places no restrictions on the ability of foreign advertising agencies to provide services from abroad to British companies. However, this is not the case in more regulated sectors such as financial services.

In these areas, countries are much more comfortable with foreign services suppliers if they operate out of local subsidiaries or offices established within their territory, under the oversight of domestic regulators. Where significant cross-border access is granted to foreign regulated services providers, countries tend to prefer using unilateral methods, such as equivalence, which allow them to retain the flexibility to remove access in future if foreign rules change, rather than binding reciprocal commitments such as mutual recognition agreements.

Ultimately, the openness of a country to foreign services providers rests on the risk tolerance of domestic politicians and regulators, and FTAs very seldom shift the domestic consensus. For that reason, FTAs rarely address regulatory barriers to trade in services in a meaningful way. Instead, FTAs focus on clarifying quantitative restrictions on market access (such as restrictions on the number of foreign firms allowed to supply a service, the amount of equity shares that can be held by foreigners, or the value of transactions) and under which circumstances foreign firms are treated in the same way as domestic ones. And in practice, rather than unlocking new opportunities for services suppliers, FTAs often focus on locking in existing levels of market access, to guard against it being rolled back in future. Instead, they help ensure certainty for companies, boosting their confidence that they will be able to access the market in five, ten or 20 years’ time.

How to create new opportunities and attract services investment

If the UK is to continue functioning as a services hub for Europe, and in some sectors, the world, it cannot be complacent. The UK’s decision to exit the EU’s single market will undoubtedly push some economic activity towards the EU member-states, and reduce its attractiveness as a base for investment. While doing its best to retain services access to the EU, the UK should aim to supplement its FTAs with a longer-term strategy to reduce barriers to trade in new markets.

1. Policy stability

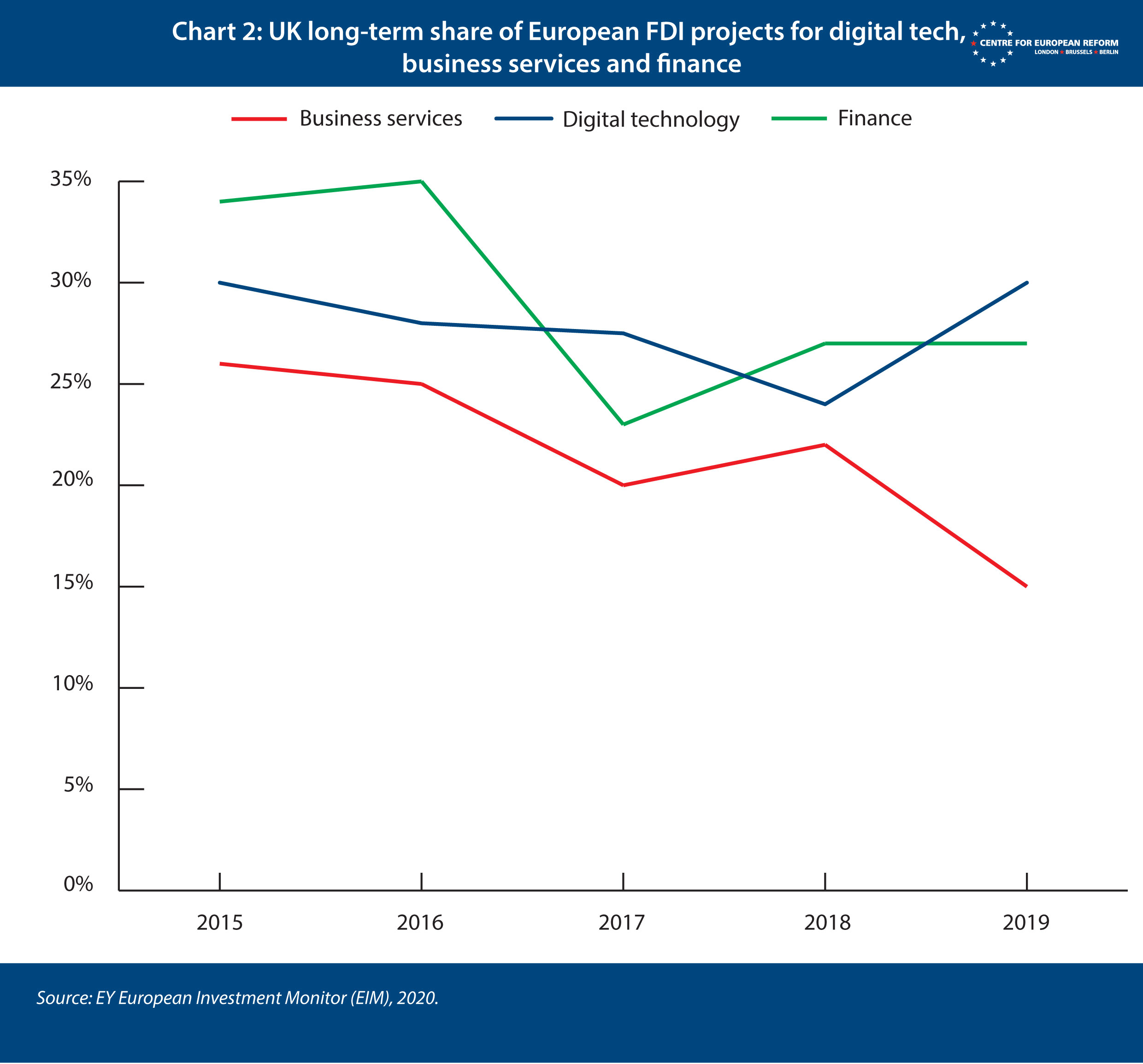

The four-and-a-half years of uncertainty in the UK that followed the Brexit vote has had a chilling effect on services investment in the UK: with the exception of digital tech, the UK’s share of European foreign direct investment (FDI) fell between 2016 and 2019 (see Chart 2). Now that the Brexit saga has concluded, with the UK choosing to pursue about as hard a rupture for the services sector as possible, British policy-makers must prioritise stability and regulatory consistency.

The UK government should ignore domestic political pressure to engage in divergence from inherited EU rules, unless there is an evidence-based rationale for doing so. Divergence could not only destabilise the UK’s trade relations with the EU unnecessarily, but also add further uncertainty for businesses that have already spent large amounts of money preparing for the changes that Brexit entailed, and managing the COVID-19 fallout.

FTAs and investment agreements potentially have a role to play. They can (to a point) bind the hands of future governments, and lock in existing levels of openness: to this effect, the UK government should also refrain from threatening to renege on recently signed international treaties.

2. Continued access to regional markets

Distance matters not only for goods trade but also trade in services – a 10 per cent increase in distance results in a 7 per cent drop in services trade – meaning that European markets will continue to be important to UK firms.8 And there are still actions the UK can take to ensure continued regional relevance.

For regulated services sectors, such as financial services, the UK’s exit from the single market involves an unavoidable loss of access. But the EU may still use its unilateral equivalence process to let some parts of the City sell services directly to EU clients. And while it is looking increasingly unlikely that the EU will grant the breadth of equivalence and subsequent levels of access that many in the UK had hoped for, this could change in future if the EU decides it is in its interest to be more accommodating, or gives up on its attempts to onshore certain sorts of financial services activity.

For unregulated services professions, such as advertising or software development, where fewer barriers to selling to EU clients exist, the UK must ensure it remains attractive as a destination for European and international talent. That is discussed in the next section.

3. Movement of people and access to skilled labour

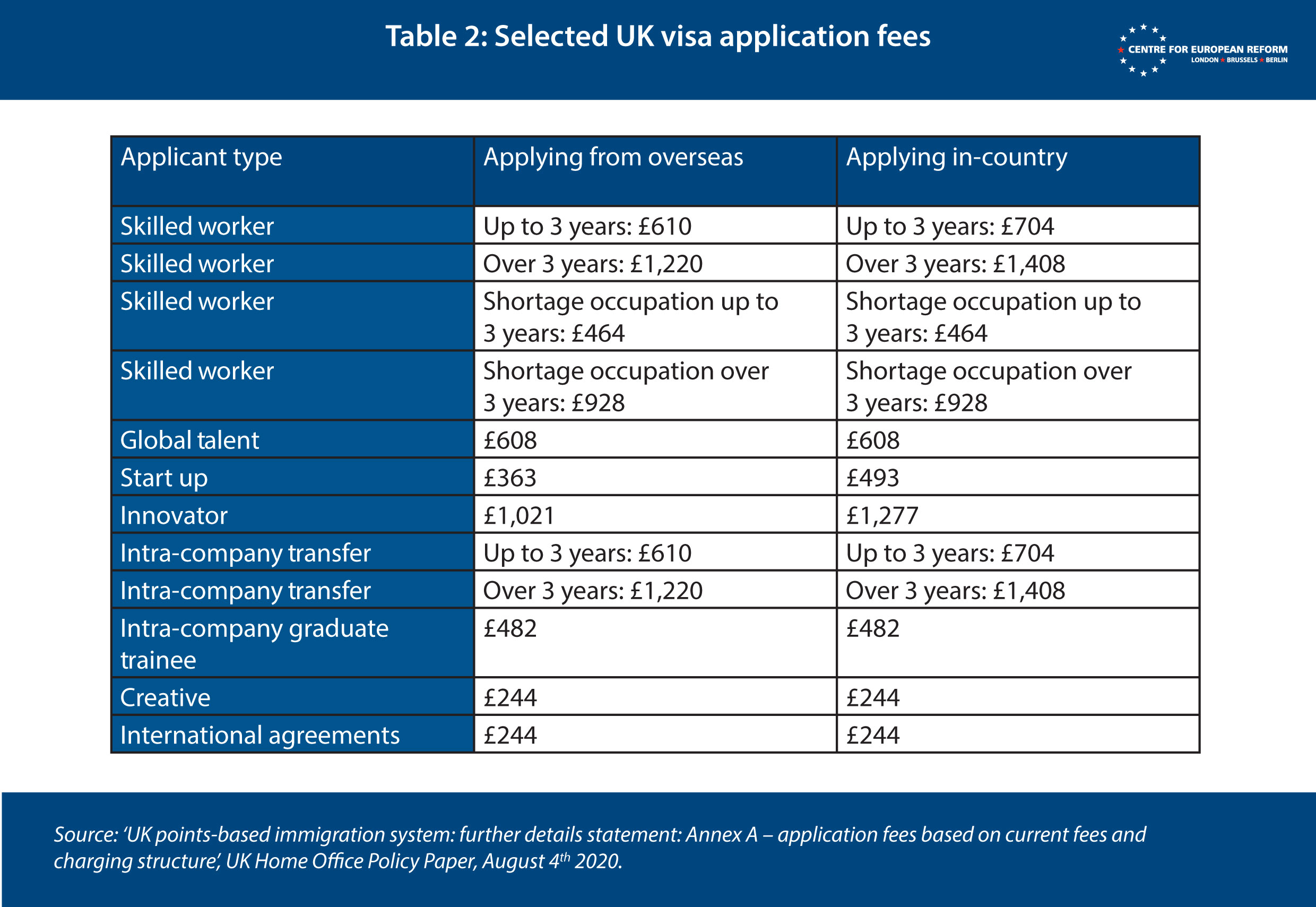

The end of free movement of people means that the UK is less open to foreign workers, even taking into account the relative liberalisation afforded to people from outside the EU under its new ‘points based’ immigration system. For British services firms, this means it will now be more difficult to attract and retain EU workers. Whereas before, EU/EEA nationals could just turn up and start working – either permanently or on a short-term basis – the prospective employer will now need to apply for a visa on their behalf, face bureaucratic hurdles and pay licence fees of up to £1,476 per worker.9 The person moving to the UK will also face expensive fees (see Table 2).10 Here, as a precursor to further liberalisation of its immigration system, the UK should consider waiving all application fees to avoid deterring workers from the EU or elsewhere. Any loss in revenue would be easily offset by the higher economic output and taxes generated by the workers coming to the UK.

Despite advances in telecommunications technology and the possibility that COVID-19 will permanently alter working patterns, services still rely heavily on in-person, face-to-face interaction. Being able to temporarily work in difference jurisdictions is a benefit for much of the professional services sector, and in investment heavy sectors such as retail franchises and utilities in particular. The UK’s rejection of freedom of movement has created problems for UK services providers with clients located in the EU. There are new limits on the activities short-term business visitors are allowed to partake in – broadly speaking a person will no longer be able to accept direct payment from their EU-based clients for whatever it is they are doing, unless they have a work permit (or an EU member-state passport). This has consequences for consultants, but also fashion models and touring musicians, for example.11

Here the UK government should drop its ideological aversion to labour mobility in the context of FTAs, and negotiate broad temporary mobility arrangements with the EU, building on the EU’s past offer to the UK, which would have allowed UK and EU residents to engage in paid work in each other’s territory for 90 days out of every 180. The UK-EU labour mobility arrangement could then form the basis of an enhanced offer from the UK to other trade agreement partners.

Some in the EU are concerned that the UK is embracing a more liberal or American approach to data flows.

4. The free flow of data

Ensuring the free flow of data should be a priority for the British government. The ability for companies to easily move personal and commercial data both in and out of the UK’s territory increases its relative attractiveness to foreign services firms. Fintech services firms are more likely to invest, for example, if they are assured that Britain will not force their algorithmic trading platform to be hosted on UK-based servers. And the UK has already demonstrated its commitment to free data flows in its trade agreement with Japan.

However, the UK needs to tread carefully. At the time of writing, press reports suggest that the EU will grant the UK so-called ‘data adequacy’ and continue to allow for the personal data of EU citizens to be stored and processed in servers located in the UK.12 But the adequacy decision is to be reviewed every four years to ensure the privacy of EU citizens is not at risk. The adequacy decision will also possibly face legal challenge, as happened when the EU put in place similar provisions for the US. If adequacy is not granted, or were to be withdrawn at a later date, it would limit the ability of UK-based companies to work with EU-wide data sets, which would make the development of artificial intelligence, for example, harder.

While the UK, as a recent EU member, currently has an approach to data that is technically compliant with EU rules, this could change in the future as UK and EU approaches evolve. And politics will inevitably influence future EU decisions in this space. Some in the EU are concerned, for example, that the UK (as demonstrated by the provisions in the UK-Japan FTA, and its desire to join the CPTPP, a plurilateral trade deal between 11 countries, including Australia, New Zealand, Vietnam and Japan) is embracing a more permissive approach to data flows, and that London will work with other countries to set global norms in digital trade, distinct from the EU’s privacy-focused approach. It is possible to have a foot in both camps – both Japan and New Zealand have EU adequacy decisions, while signing up to liberal digital provisions in their FTAs – but proximity and heightened political attention might make it more difficult for the UK to continually satisfy EU decision-makers.

Internationally, the UK will need to work with like-minded partners to ensure that the existing World Trade Organisation (WTO) moratorium on levying customs duties on electronic flows endures. Countries such as India and South Africa argue that the moratorium has had a “catastrophic impact” on growth and jobs in developing countries, alongside the erosion of tariff revenues.13 Technological advancements in areas such as 3D printing in manufacturing will only lead to increased opposition, as some taxable goods stop crossing borders physically. The ongoing plurilateral e-commerce negotiations being held between a number of WTO members would make the moratorium permanent for participants, but they are unlikely to conclude anytime soon.14 The UK could use its FTAs to create a network of the willing, and lock in binding commitments on the free flow of data.

5. Regulatory diplomacy

Tearing down cross-border barriers to trade in services requires trust: foreign regulators need to be convinced that UK rules and enforcement provisions are as effective as their own. Developing official channels of communications, and building strong working relationships takes time and effort. But in the long-run, continued dialogue can ensure that new barriers to trade do not emerge, and encourage countries to unilaterally remove those that currently exist.

Regulatory diplomacy can occur in a number of different forms, both formal and informal. The continuing discussions between the UK Treasury and the Swiss finance ministry on the mutual recognition of rules in financial services is an example of a formal process that could bear some fruit in the future.15 Britain’s dialogue on financial services in its FTA with Japan is less ambitious than the one with Switzerland, but could still benefit UK and Japanese financial services firms in going forward if it leads to more stable and predictable regulation for firms in both countries.

On the mutual recognition of professional qualifications, FTAs (including those with the EU and Japan) offer little more than commitments to keep talking. Here the UK will need to work with foreign governments, and certification bodies in both the UK and abroad, and cajole them into recognising the respective qualifications of architects, engineers and others. While this should be relatively easy on paper, it often proves difficult because the respective qualifications bodies are unwilling to erode their domestic monopoly power by allowing foreign entities to provide the same certification service. Again, progress in this area will be slow, but if successful it can unlock opportunities for UK-based services providers seeking to export their skills.

Conclusion

To make the most of future opportunities to grow its traded services sector, and retain its global standing, the UK’s domestic discussion on trade in services will need to mature. Removing barriers to trade in foreign markets will remain difficult, and require long-term regulatory efforts to build trust and understanding. One-shot FTAs might make for good headlines, but they largely protect the status quo rather than unlocking new opportunities for services exporters. Policy-makers should focus on attracting – and retaining – the investment of international services firms into Britain. More than anything, the UK government needs to convince investors that recent policy instability is a thing of the past, that it remains open to ideas and people, and that it is still a great location from which to reach out to clients across the EU and beyond.

2: Andreas Maurer and Steen Wettstein, ‘TiSMoS – a new global trade in services data set: What the modes of supply can tell us’, WTO, November 20th 2019.

3: Ingo Borchert and Julia Magntorn Garrett, ‘Foreign investment as a stepping stone for services trade’, UK Trade Policy Observatory, June 11th 2020.

4: Sam Lowe, ‘Brexit and services: How deep can the UK-EU relationship go?’, CER policy brief, December 2018.

5: ‘UK-Japan comprehensive economic partnership agreement’, Department for International Trade, October 23rd 2020.

6: Liz Truss, ‘Opening statement for the UK-Japan agreement in principle’, Department for International Trade, September 11th 2020.

7: ‘The UK-Japan Comprehensive Economic Partnership: Benefits for the UK’, Department for International Trade, October 23rd 2020.

8: John Springford and Sam Lowe, ‘Britain’s services firms can’t defy gravity, alas’, CER insight, February 5th 2018.

9: ‘UK visa sponsorship for employers’, HMG, 2021.

10: Jonathan Portes, ‘Brexit and beyond: Immigration’, UK in a Changing Europe, January 19th 2021.

11: Sam Lowe, ‘The post-Brexit trials and tribulations of the touring musical troupe’, Encompass, January 2021.

12: ‘Brussels to allow data to continue to flow to UK’, Financial Times, February 15th 2021.

13: ‘WTO members highlight benefits and drawbacks of e-commerce moratorium’, IISD, July 23rd 2020.

14: ‘WTO; e-commerce negotiations: A unique opportunity for digital trade’, DIGITALEUROPE, October 22nd 2020.

15: ‘Joint statement between Her Majesty’s Treasury and the Federal Department of Finance on deepening co-operation in financial services’, HM Treasury, June 30th 2020.

Sam Lowe is a senior research fellow at the Centre for European Reform

February 2021

The author is grateful to Hosuk Lee-Makiyama, whose writing and comments on the relationship between services and investment inspired many of the arguments made in this paper.

View press release

Download full publication