How to make EU fiscal rules compatible with net zero

- Businesses, households and governments in the EU must invest more in green energy, infrastructure and energy efficiency to meet Europe’s climate goal of net zero greenhouse gas emissions by 2050. That will require additional annual investment of around 1.7-2 per cent of GDP. If big extensions to public transport networks are needed, the investment figure will be higher still.

- Big investments in power generation and heating homes are largely uncontroversial, and the need to stop buying Russian energy makes them more urgent. A carbon price already applies to power generation under the EU emissions trading scheme, and the path to climate neutrality in energy is relatively clear. The technology for green housing is also largely mature and well-established.

- The magnitude of investment needs in transport is more uncertain. Electric vehicles are entering the market in growing numbers; the current price spike for petrol will only accelerate the rollout. If technology improves quickly so that trucks and planes can be electrified, a costly reset of Europe’s transport system may not be needed, and Europe can instead gradually replace vehicles, ships and planes. If not, governments will have to expand railway networks – an expensive endeavour.

- Industrial investment costs are high but could be reduced by technological progress. Greening industrial heating is comparatively easy as green alternatives to natural gas exist, albeit costly ones. In response to current gas prices, the private sector will invest more in these technologies. But ‘process’ emissions that are unrelated to the burning of fossil fuels, such as emissions released when making cement, are much harder to avoid, or to capture and store underground.

- The private sector must undertake most of the investment to tackle climate change. But the public sector will have a role to play, too. If the EU does not ensure a carbon price that is high enough to make green investment worthwhile, the public sector will have to subsidise private investment, or enforce it through stiff regulation. It will also have to cushion the blow to poorer households’ finances from higher energy prices, and invest in regions with lots of brown industry to help them find new business models.

- Green public investment in Europe is on the rise, both nationally and at the EU level, thanks in part to the EU’s recovery fund. But there remains a sizeable gap against what is needed. A back-of-the-envelope calculation shows that Italy will have to finance with its own budget 1.1 per cent GDP per year more to reach the 2030 climate goals, Spain 1.3 per cent of GDP and France 1.2 per cent of GDP.

- There is little hope that these large spending needs can fit into the EU’s current fiscal rulebook. At the same time, some countries are highly indebted and cannot increase debt much further. A compromise could see a country-by-country EU review process that allows some green investment to be exempted from the EU’s rules, and some financed by higher taxes or cuts to other spending.

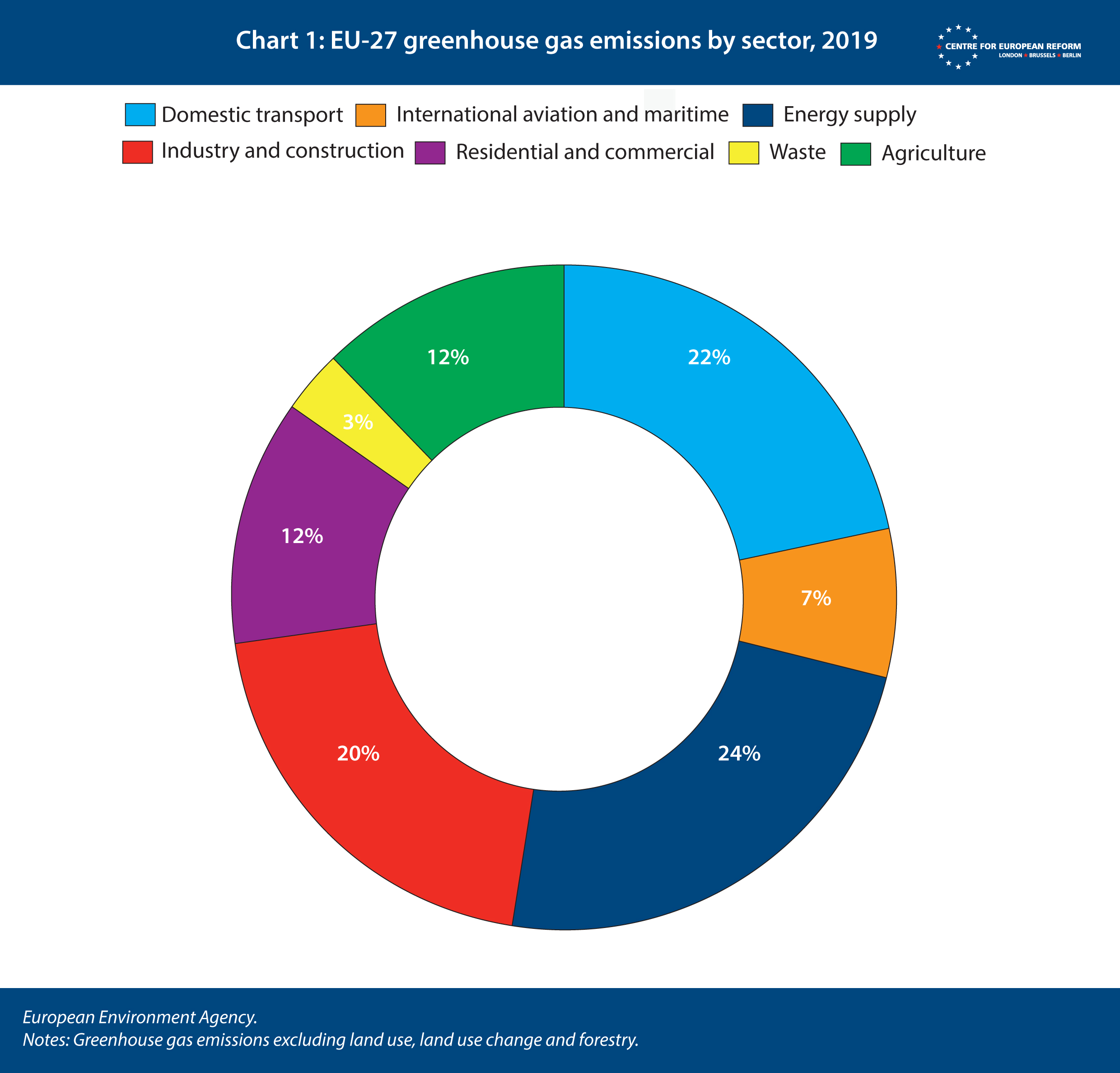

While the EU aims to achieve net zero greenhouse gas emissions by 2050, its economy is still heavily dependent on fossil fuels. But in many sectors, the technology to reduce emissions drastically is already available and sometimes cheaper than technologies currently in use. The power sector still emits around 760 million tonnes of carbon dioxide per year, even though renewable energy generation is in many cases already cheaper than generation from fossil fuel-powered plants (see Chart 1).1 Transport is still a large contributor to carbon emissions in Europe but, sales of electric vehicles are growing rapidly. Heating buildings accounts for 317 million tonnes of carbon emitted each year, though heat pumps and insulation could save money for consumers, especially now that higher gas prices are here to stay.2 Existing clean technology is still too expensive to be commercially available only in some transport sectors (long-haul air travel and shipping) and some industrial sectors (such as cement production).

What is needed to cut emissions rapidly is more green investment. Most of the investment has to be undertaken by the private sector. But considering the scale of the investment needed, and the timeline to meet Europe’s climate targets, public money will be necessary to speed up private investment and to subsidise R&D and innovation in areas where technology is currently unviable. The state will also need to make sure that public infrastructure is adapted to shift away from fossil fuels. During the transition, vulnerable households will need financial support to avoid energy poverty. The Russian war on Ukraine only increases the urgency with which Europe must become less dependent on Russian fossil fuels – not only natural gas, but also oil and coal.

At the same time, Europe’s fiscal rules put limits on deficits that governments can incur. During the pandemic, the rules were suspended, to allow countries to spend big to help workers, firms and families get through the crisis. The plan to reinstate the rules has been all but shelved for now, as Russia’s war on Ukraine is hitting the European economy. Higher investment in defence is needed, on top of stimulus for pandemic recovery and green investment. But at some point, the fiscal rules will have to be reinstated.

This policy brief looks at the investment that Europe needs to become climate neutral by 2050, fulfill its 2030 targets along the way and wean itself off Russian energy imports. It then considers how EU fiscal rules are holding such investment back, and sketches out a reform to the rules to make them compatible with net zero emissions goals.

How much investment is needed?

Almost all vehicles, buildings, heating systems and home appliances, as well as industrial structures, machines and power plants need to be carbon-free before 2050, and substantial progress needs to be made in the 2020s. This means that, across the economy, zero-carbon technologies should replace fossil fuels. The good news is that advanced economies are innovative and consume fewer and fewer resources per unit of output, so the EU can transition to a net-zero emissions economy without a war-like mobilisation of resources or reducing living standards.

Power and transport

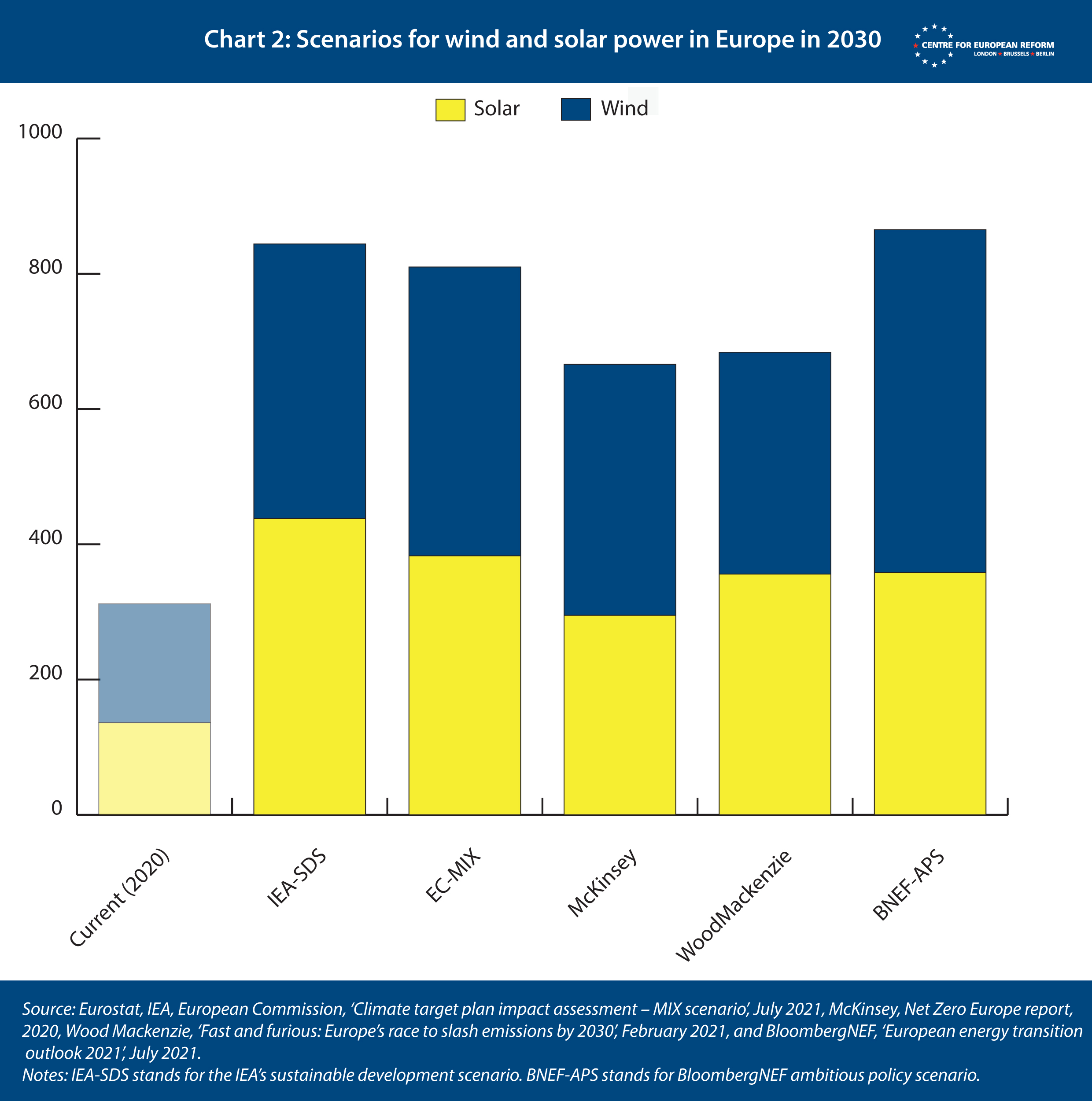

Start with the power sector. The amount of renewable power the EU will need in order to achieve its 2030 climate target is staggering. Electricity consumption will increase significantly as road transport and the heating of buildings are electrified. According to analysis by the European Commission, around 250 GW of wind power and 245 GW

of solar capacity must be added by 2030 to meet the emission reduction targets (Chart 2).3 That means total installed capacity of solar and wind power should rise by 50 GW per year over this decade, while only 20 GW per year were added in 2016-2020, according to Eurostat.

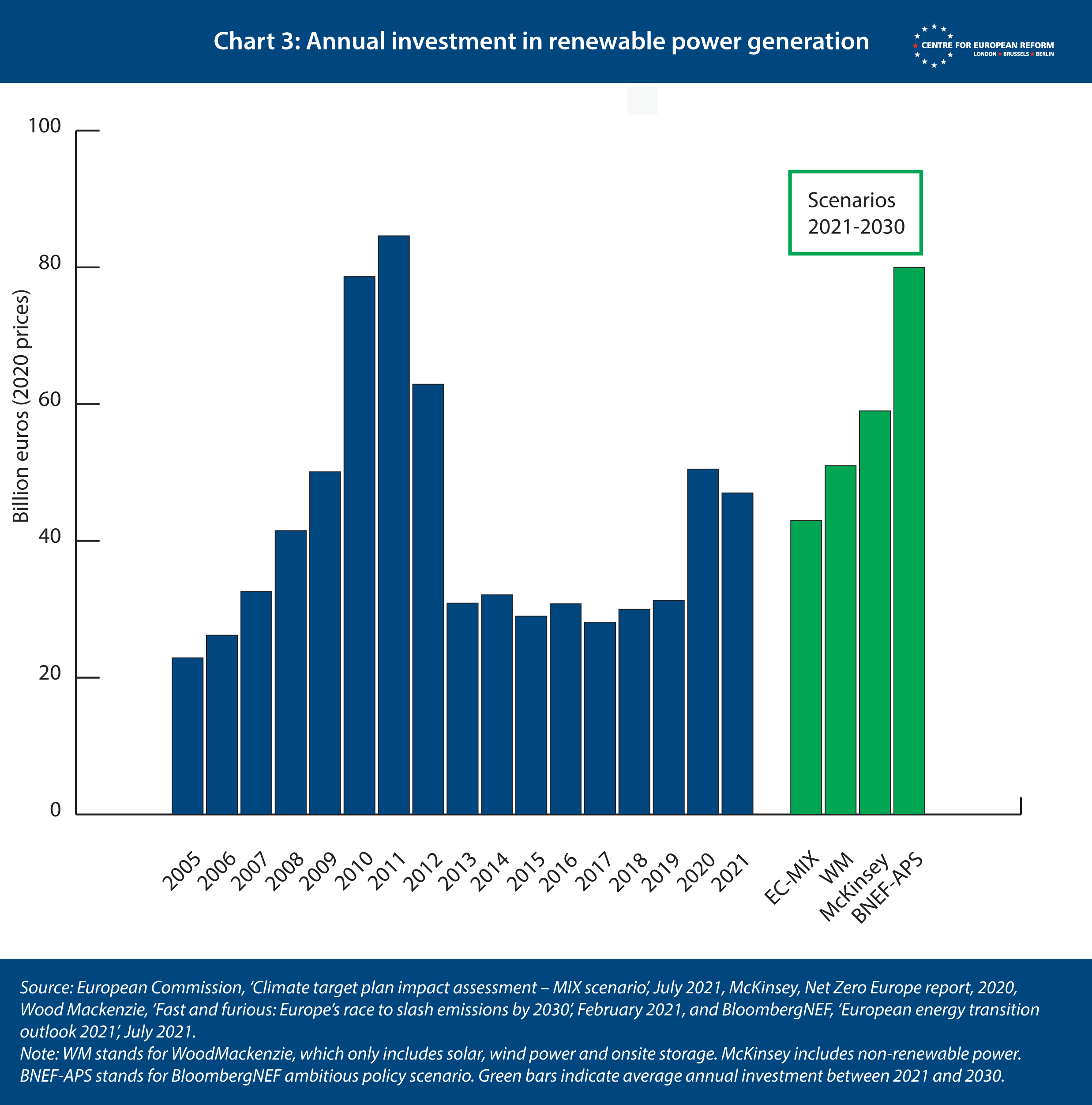

But this does does not mean vast increases in expenditures in power generation are needed before 2030, in terms of money spent (Chart 3). In the past ten years, the cost of generating electricity from solar and onshore wind energy has dropped by 85 and 56 per cent respectively, making onshore and offshore wind as well as utility-scale solar power increasingly competitive with fossil-fueled power stations.4 This means that Europe gets more generating capacity per euro invested than before. European power generators spend vast amounts each year to build new plants or replace and refurbish old ones. As shown in Chart 3, estimates by the European Commission, McKinsey, the International Energy Agency and WoodMackenzie each suggest that annual investment spending on renewable power plants throughout this decade only needs to increase by €10-25 billion from the 2015-2021 average. BloombergNEF, a research firm, projects higher investment needs, with a rise of €45 billion.

But even that would be manageable, as it would just require Europe to return to the level of the 2010-2011 boom in investment in renewable installations.

However, Russia’s war on Ukraine means higher investment must happen quickly. The European Commission’s initial proposal the ‘REPowerEU’ plan aims to phase out all Russian energy imports by 2027 and to bring investment in renewables and green hydrogen forward.5 The plan calls for the annual deployment rate of solar and wind power generation to rise by 20 per cent compared to the current targets under the Fit for 55 plan. It calls for 15 TWh of rooftop solar power generation to be added this year. More green hydrogen will be needed, in part to directly substitute for natural gas. As electrolysers used to produce green hydrogen are electricity-intensive, the Commission estimates that 80 GW of renewable power capacity will have to be installed for this purpose.

A similar story can be told about electric vehicles (EVs). The price of lithium-ion batteries, essential for EVs and energy storage, has fallen considerably, and BloombergNEF expects the price of EVs to be in line with combustion engine cars in all passenger car segments in Europe by 2027. Car sales in Europe in the third quarter of 2021 were already 10 per cent electric, and another 30 per cent were some form of hybrid with both an electric motor and a combustion engine.6 This rapid shift should deliver most of the emission reductions needed from non-commercial road transport.

In both power and transport, a lot more investment in infrastructure is needed: to store and distribute clean power, to charge electric vehicles, and in public transport. Take the power system. Using intermittent renewable generation requires significant investment in the grid, to make sure regions with lots of wind or sunshine can supply regions with little, to balance daily and seasonal power needs. The grid and distribution system also need to allow storage like batteries or hydrogen production, to add additional balancing capacity. Annual power grid investment in 2021-2030 will need to be €32 billion higher than in the last decade, according to the European Commission.7 In other words, more additional investment is needed in the grid than in power generation capacity.

In transport, EVs need a large and dense network of charging points, private and public. Luckily, the associated investment is manageable: BloombergNEF estimates that in order to accommodate a share of 18 per cent of EVs on the road in 2030, a figure in line with the EU climate targets, €10 billion per year would be needed across the whole EU.8 High petrol prices may speed up the sale of EVs, in which case the charging infrastructure would need to grow faster. Rail and shipping capacity will also have to grow to shift passenger and freight transport away from road and aviation. City administrations need to expand public transport and cycling infrastructure to encourage alternatives to cars, as the switch to EVs will take time and does not solve the problem of urban congestion. Finally, the large increase in hydrogen demand for long haul aviation and shipping will require investment in hydrogen distribution networks.9

Even very high investment in renewables would be manageable, as it would just require Europe to return to the level of the 2010-2011 boom.

There is great uncertainty about how much investment is needed for transport infrastructure. The transport sector accounts for 35 per cent of the €390 billion that the Commission identified as additional investment needs for 2021-2030.10 This estimate covers the higher prices of clean vehicles and the rollout of recharging infrastructure, but it does not include investment in new rail tracks, public transport or cycling infrastructure. Separately, the Commission estimates the investment gap for international, inter-urban and urban transport at €110 billion per year (in 2020 prices).11 This extra investment might be needed to cut transport emissions, depending on the pace of green innovation in road, air and maritime transport. Shifting passengers from one mode of transport to another is an expensive way to cut emissions, but it may be necessary in countries that have underdeveloped transport infrastructure.

Housing

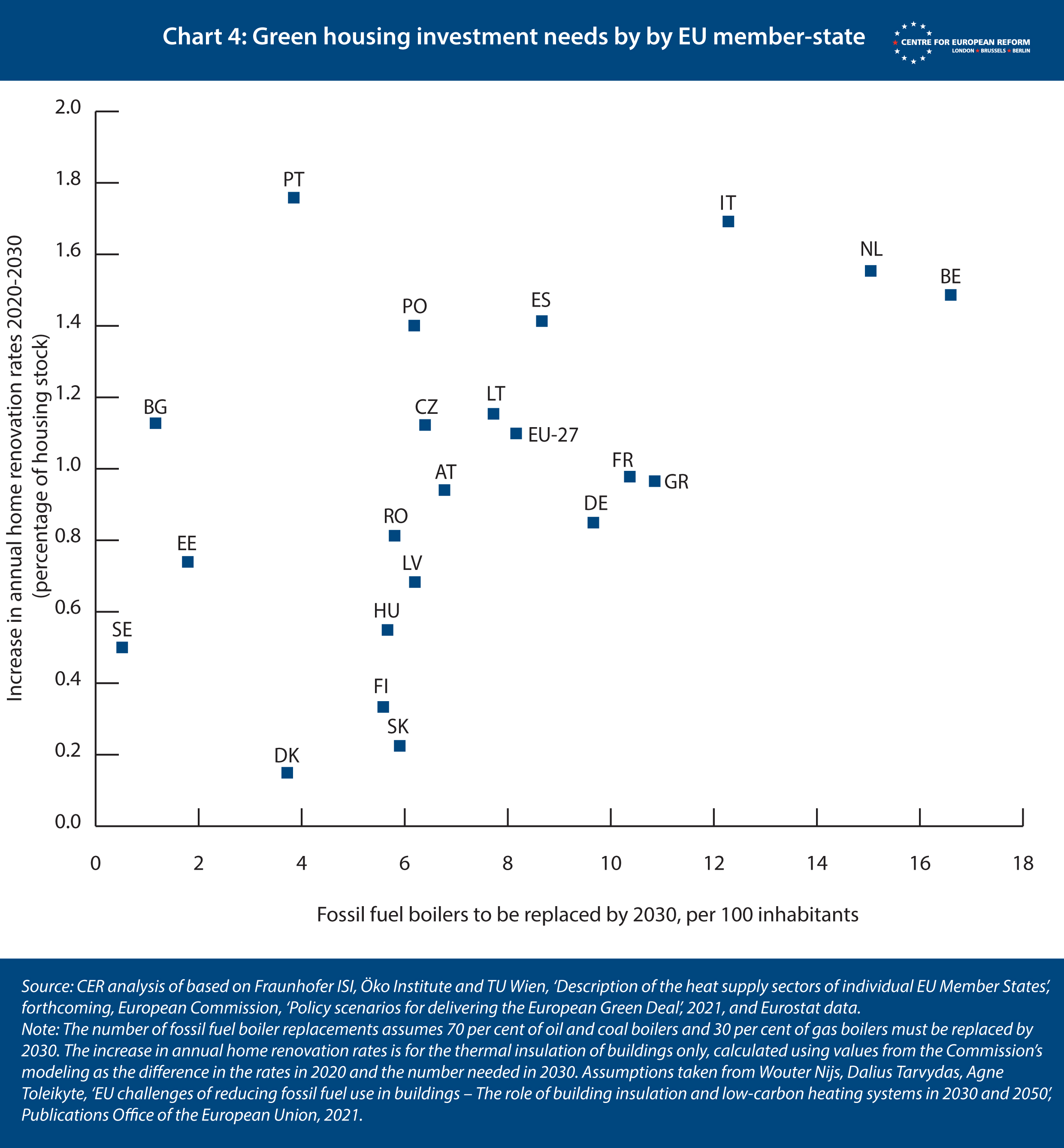

The housing sector has the largest investment needs in the EU because the share of retrofitted houses is still low, and because renovation costs continue to be relatively high: there is less potential for standardisation and economies of scale in construction than in manufactured goods. According to Commission calculations, the current annual rate of green housing renovations will have to improve – from 0.9 per cent to 2.1 per cent of the housing stock by 2030 – and retrofits must be more comprehensive. ‘Deep’ renovations, delivering energy savings of at least 60 per cent, should rise from 0.2 per cent of dwellings each year to 1.3-1.7 per cent in 2030. Total investment in the greening of buildings should reach around €300 billion per year by 2030, twice the current levels.12 Chart 4 shows the necessary increase in renovations on the vertical axis, and the need to replace fossil fuel boilers on the horizontal one. The further a country is to the top right, the more green investment in housing is needed.

Industry

The industrial sector will need a lot of investment too. For example, in cement production over half of the emissions do not stem from burning fossil fuels to create heat but are released from the limestone used to produce clinker. Carbon emissions from ndustrial processes need to be drastically reduced or captured and stored underground, which is complex and expensive.

Heavy industry plants typically last from 20 to 70 years. That means that, to avoid locking in emissions, companies must switch to climate-friendly alternatives when plants are reaching the end of their lifetime and need to be refurbished. Around 40 per cent of existing plants and machines in the European cement, steel, and chemical sectors are up for major reinvestment or renewal by 2030.13 Most of the green technologies to replace them have passed the demonstration phase, but to be profitable many sectors need carbon prices to be higher than €100/tonne, or public subsidy. Technological progress is still highly uncertain, and so are public subsidy needs.

Investment gap

The upshot is that investment needs differ by sector, but the total is substantial. The investment needs of the power and buildings sectors are largely uncontroversial, in transport estimates start to diverge considerably, while in the industrial sector, there is still a lot of uncertainty about technological progress, which does not allow for very confident estimates. Both the Commission and McKinsey put the additional annual investment in the 2020s in the range of €250-300 billion (1.7-2 per cent of 2019 GDP) for all sectors except transport, relative to the annual investment average over the last decade. Roughly 70 per cent of this spending will be in the construction sector.14 In transport, the Commission puts the investment gap on clean vehicles and recharging infrastructure at €135 billion per year (1 per cent of 2019 GDP), with rail and public transport investment of €110 billion coming on top.15 Others have a much more optimistic view on technological progress in transport, and hence much lower investment figures. These estimates do not consider other priorities of the European Green Deal, like the circular economy, water management and biodiversity, which require additional annual investment of around €130 billion across the EU over the current decade, according to the Commission.16 Investment on climate change adaptation – flood defences and sea walls, for example – should be added on top.

Why is there a role for the public sector?

As the climate economist Sir Nicholas Stern put it, climate change is the result of the greatest market failure the world has ever seen. Carbon emissions had no or a low price tag until recently, so the private sector had little to no incentive to reduce its carbon footprint. Digitisation and other innovations tend to reduce the amount of emissions for each euro of GDP. But that benefit is at least partially offset by the economic growth – and therefore emissions – that these technologies bring.

Governments have an important role in making sure the transition to net zero is fair, to maintain political support for decarbonisation.

The green innovations offering the steepest reduction in emissions, like low-carbon industrial processes, are expensive. Firms do not voluntarily adopt them without financial support, or unless the polluting alternative is made equally expensive through carbon pricing, or phased-out through regulation.

The recent surge in carbon prices in Europe is changing firms’ behaviour: in February 2022, prices for emissions permits on the European Emissions Trading System hit close to €100 per tonne of carbon. However, Russia’s war on Ukraine has lowered them back to around €60 per tonne, as a weaker economy that is trying to wean itself off currently expensive Russian fossil fuels is bound to emit less carbon for a while. A rise back to €100 per tonne would make some required investment more profitable, but according to McKinsey it would still leave almost 20 per cent of the needed investment without a positive business case.17 Public financial support to change that could take the form of cheaper lending, direct subsidies or taking on some of the risk that private investment and innovation brings with it.

Many private investments can also be made more profitable if the state provides the infrastructure to support them. Private rail lines need rail tracks to connect travellers with cheap and fast services; a large network of charging stations makes selling electric vehicles a lot easier; and an electricity grid that can stomach intermittent power plants and incorporate decentralised storage, like batteries, invites more investment in renewable energy or smart meters. Some of that infrastructure could be privately provided, of course, as the electric car maker Tesla is demonstrating with its network of charging stations. But often, there is a chicken-and-egg problem: without infrastructure there will be no customers, but without customers there is no incentive to build the infrastructure. The public sector does not have that problem, and can invest in infrastructure that is open to all businesses that want to use it.

There are further barriers to private investment. Small and medium-sized enterprises may struggle to find funding for a risky green project. Administrative hurdles and planning permits further complicate the investment process for firms and households. Solar and wind power have become cost-competitive in many areas of Europe, and even more so with higher carbon prices. But their roll-out is severely slowed down by planning restrictions restrictions on the location of plants and the time it takes to get permits.

Governments have an important role in making sure the transition to net zero is fair, to maintain political support for decarbonisation. The current period of high gas, oil and electricity prices is a good example: governments must cushion the shock to household finances. Governments may also have to provide more support for low-income households to renovate their home or replace their car, in order to shield them from higher fossil fuel prices. This is the aim of the proposed new EU Social Climate Fund, of about €140 billion.

Governments will also have to support regions that are most hit by the green transition, for example coal-mining regions or those with a lot of heavy industry. Germany allocated €40 billion of its coal phase-out plan to support the affected regions. The new EU Just Transition Fund dedicates around €20 billion to the same purpose.

Beyond Europe, the EU will have to boost its support for low-income countries if it hopes to make further progress on international climate negotiations, and to help these countries adapt to climate change. Moreover, an EU Carbon Border Adjustment Mechanism could well hurt the least developed economies that are dependent on exports to Europe and cannot rapidly switch to low-carbon manufacturing technologies.18 Some form of compensation may be necessary here, too.

The total fiscal cost to European countries of addressing climate change is hard to boil down to one number. Too many policy and technological variables are simply unknown. How willing will governments be to tighten regulation and increase the carbon price, instead of showering the private sector with money to spur climate investment? How much has the energy price surge and the Russian war on Ukraine focussed minds on climate investment? How fast will technology improve in some of the hardest-to-abate sectors?

With these caveats in mind, the required EU-wide increase in public investment and spending for climate change mitigation, compared to the last decade, should be around €150 billion per year (around 1 per cent of GDP).19 Public investment in rail and public transport infrastructure would add another €100 billion per year (around 0.7 per cent of GDP).

How much are national governments investing?

Over the last two decades, the EU and national governments have supported low-carbon energy innovation and green investment. The EU is financing pan-European research (the Horizon Europe programme) and trans-national energy and transport infrastructure projects such as gas pipelines between EU countries (the Connecting Europe Facility).20 Between 2014 and 2020, the EU aimed to spend 20 per cent of its budget on investment projects that directly contribute to climate action, worth €30 billion per year on average.

Total European climate investment is therefore on an upward path, but the RRF is not permanent, and a gap remains.

The new EU 2021-2027 budget has boosted spending on climate action from €30 billion to at least €45 billion per year. The debt-funded EU recovery fund (Recovery and Resilience Facility, RRF) gives financial firepower to poorer member-states to increase their climate investment until 2026. At least 37 per cent of recovery fund spending has to directly contribute to climate action. According to the European Commission, national governments are allocating €177 billion from the RRF to climate-related programmes in the 22 approved recovery plans, amounting to roughly €29.5 billion per year.21

At national level, renewable energy support schemes such as feed-in tariffs have been the biggest climate expense over the last two decades. Payments for such schemes in 2019 alone were around €72 billion across the EU.22 Often financed through electricity surcharges paid by consumers, they have contributed to the rapid roll-out and falling costs of renewable power generation.

But overall, government spending on climate change mitigation has so far put little burden on national budgets. In 2019, total national public spending in the EU in the areas of pollution abatement (including tax-financed subsidy schemes for renewable energy) and environmental R&D was just €23 billion, according to Eurostat.

Total European climate investment is therefore on an upward path, but there are two problems. First, the RRF is a one-off measure and it remains unclear whether countries that are net payers are willing to repeat transfers to the south and east, even for an important public good like climate protection. The war in Ukraine is adding a security angle to climate investment, which will help make the case for another RRF, but a permanent system of transfers still faces big political obstacles.

Second, a sizeable spending gap remains if Europe is to reach its 2030 and 2050 climate goals, even with the RRF funds. With a back-of-the-envelope calculation and subtracting the fresh resources from the new EU budget and the RRF, Italy will have to finance 1.1 per cent of GDP per year of additional public expenditures, Spain 1.3 per cent of GDP and France 1.2 per cent of GDP. The key question for the fiscal policy debate in Europe is how to plug that gap over the medium and long term.

How European fiscal policy should plug the investment gap

European fiscal policy-making is guided by rules, which have by now become so complex that it is hard to implement them. Those rules have also had a single-minded focus on stabilising debt levels and containing deficits, so that more complex tasks – such as ensuring a healthy climate, safeguarding the recovery from a recession or generating inclusive growth – were left out. But with a sizeable spending gap on climate, high debt levels as a result of the pandemic, a war in Europe and inflation running high, it is increasingly clear that Europe’s current fiscal rulebook is unfit for the future.

It is true that fighting climate change can generate revenues. The EU Emission Trading System (ETS) for the power and industry sectors has generated €11.4 billion in auction revenues for national governments in the first six months of 2021 and it could offer annual income worth €30 billion per year through 2030, according to our calculations. The new EU ETS proposed by the European Commission, which will extend carbon pricing to road transport and buildings, could generate €48 billion (0.3 per cent of GDP) extra revenues per year in 2026-2030. National environmental taxation is also creating revenues.

Fighting climate change can generate revenues, but governments are also bound to face declining revenues from fossil fuels.

Some of that revenue, especially from the ETS on heating and transport, will have to be redistributed to citizens, and to lower-income households in particular. And ETS revenues are lower than they could be: to protect domestic industries from trade partners that do not face stiff environmental regulation and carbon pricing, the ETS has been granting free allowances to energy-intensive and trade-exposed sectors like cement and steel. With ETS prices averaging €55 in 2021, lost revenues from free allowances were worth €36 billion last year. It is still uncertain whether the introduction of the Carbon Border Adjustment Mechanism – in effect a carbon tariff on some goods from countries with no or low carbon prices – will end this subsidy to industry.

National governments could also find additional revenues by eliminating fossil fuel subsidies. According to the European Commission, subsidies for fossil fuels in the EU were worth €56 billion (0.4 per cent of GDP) in 2019.23 Proper ‘green budgeting’ – a system that assesses the environmental impact of a state’s budget – could also make green spending more efficient, refocusing public programmes towards the most carbon-saving activities. For example, governments should consider eliminating some of the tax credits for light home renovations, and redirecting these funds towards more comprehensive renovations, as Germany has recently announced it will do.

But governments will also lose revenues from taxing fossil fuels, for example when citizens switch to electric cars. Fuel tax generates 3 per cent of GDP in revenues in Greece, and 2.1 per cent in Italy. Electric cars should make up around 20 per cent of the stock of passenger cars by 2030, according to the Commission’s Fit for 55 and IEA’s Sustainable Development scenarios. The UK’s Office for Budget Responsibility (OBR) shows how these losses in fossil fuel tax revenue will increase exponentially after 2030, outweighing carbon pricing revenues by the end of the 2030s. The first goal of Europe’s fiscal policy should thus be a comprehensive green review of its revenues and spending, to maximise the decarbonisation impact of government policies, and to make that review part of its fiscal governance.

Second, fiscal rules need a climate investment exemption. Under current rules, countries with high debt levels will have to cut back on spending or raise taxes to reduce their debt levels over time. Before the pandemic, in 2019, Italy just barely complied with the fiscal limits set out in the rules, and only after some back and forth with the Commission. A global pandemic and a European war later, Italy will only be able to comply with the rules with very strict budget discipline that leaves little room for large investments. Both the Commission and the International Monetary Fund (IMF) saw significant risks to Italy’s debt sustainability before the war, and they are only higher now.24 Debt sustainability in a monetary union is a common good.

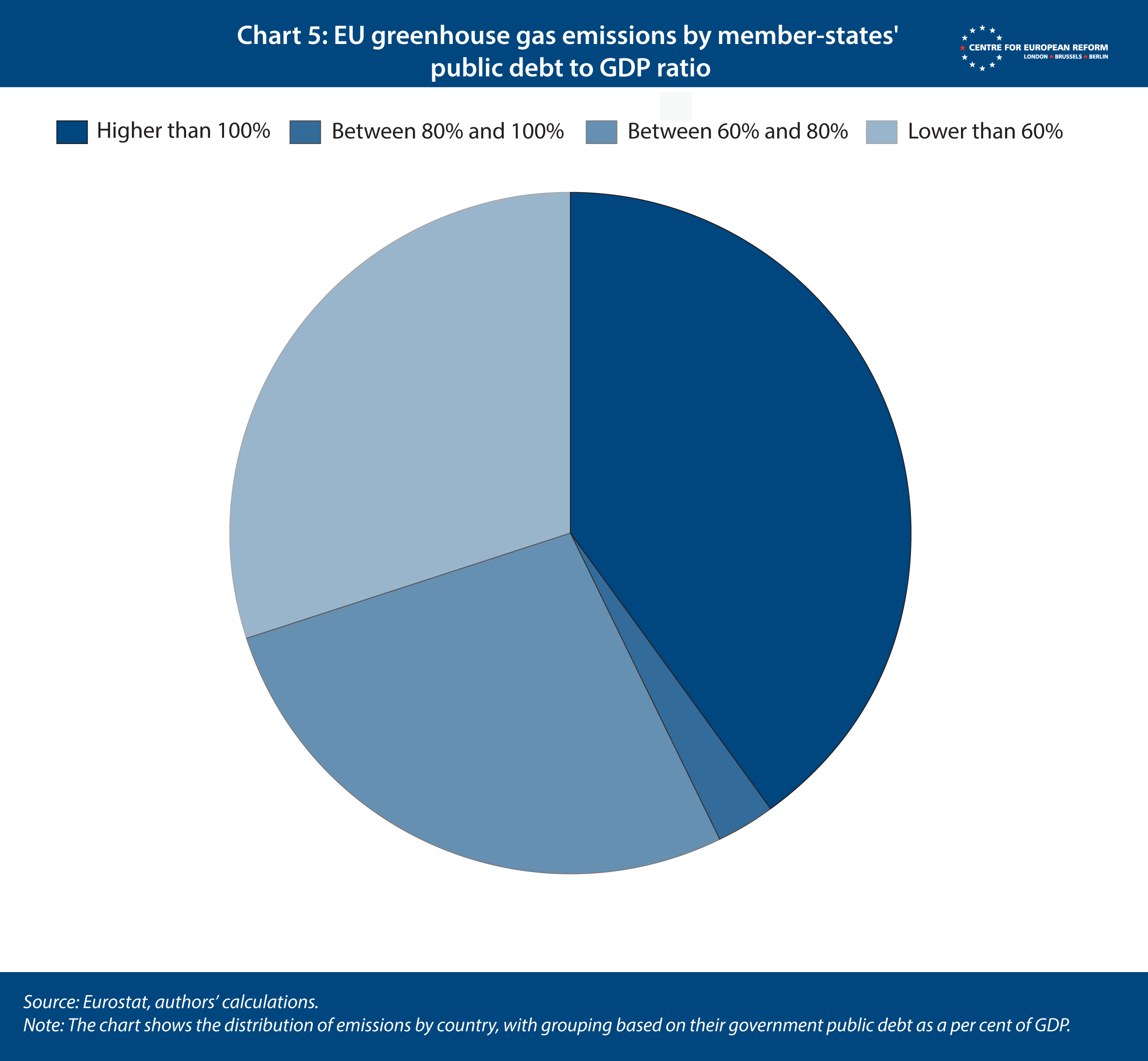

Defenders of the rules also argue that compliance with the rules in the past created the fiscal room to spend in crises and invest in climate action. That argument has merit: Germany or the Netherlands can easily mobilise the additional spending needed to tackle climate change within the rules, while Italy or Spain cannot without significant cuts to other spending. But given high debt levels, the mandate to reduce deficits and debt will invariably lead to cuts, and investment is likely to be one of the first to go.25 As countries with high debt levels are responsible for a large share of Europe’s carbon emissions, they need some fiscal room to invest (see Chart 5).

There is no easy solution to this problem. Giving highly indebted countries too much leeway in the form of a blanket exception on all green spending (a ‘green golden rule’) is a political non-starter, as northern hawks will argue that too much spending could then be classified as green. What is more, Europe’s high-debt countries will have to cut back on some other spending items in their budgets, and will not be able to fund green investment entirely through new debt.

A better approach is to start with the policy goal: the climate investment needs of each country. There are two institutional arrangements to build on: the national recovery plans in the RRF, in which countries spell out their reform and investment plans to unlock recovery fund money; and the national energy and climate plans in which countries described their plans in 2018 to reach the EU’s climate goals, and which require regular progress reports since.

To then tweak the fiscal rules, countries could, in a first step, submit their climate investment needs and plans, for review and approval by the Commission and the Council. In a second step, the Commission would compare those green investment needs by the money spent on fossil fuel subsidies or lost on inefficient green spending. After all, countries that can afford fossil fuel subsidies can also afford to fund climate investment within the limits of the fiscal rules. The resulting figure would be further reduced to account for the share of grants received via the RRF and the EU budget that are dedicated to climate investment, as those green investments are already funded via EU transfers. The final amount would then be the climate investment left that would be exempted from the deficit rules, subject to regular assessments on countries’ progress in their climate investment plans.

The current setup of the EU’s fiscal rules would not allow for such exemptions, so legislative changes would be needed. But an opening of the rules for climate investment purposes would be in the interest of more frugal countries in the North. Climate investment is a common good in Europe, and the investment needs are large. The recovery fund should be made permanent, to allow some of that investment to be funded through common European borrowing. But Europe’s fiscal rules need to accommodate some of the rest, to make sure Europe can reach its climate goals without political crises.

2: Source: Eurostat. The value refers to 2019.

3: European Commission, ‘Climate target plan impact assessment – MIX scenario’, July 2021.

4: IRENA, ‘Renewable Power Generation Costs in 2020’, 2020.

5: European Commission, ‘REPowerEU: Joint European action for more affordable, secure and sustainable energy’, March 2022.

6: BloombergNEF, ’Electric vehicle outlook 2021’, and ACEA, ‘Fuel types of new cars’, press release, October 2021.

7: European Commission, ‘Climate target plan impact assessment – MIX scenario’, July 2021.

8: BloombergNEF, ‘European energy transition outlook 2021’, July 2021.

9: See Agora Energiewende and AFRY Management Consulting, ‘No-regret hydrogen: Charting early steps for H2 infrastructure in Europe’, January 2021.

10: See for instance Box 2 in European Commission, ‘The EU economy after COVID-19: implications for economic governance’, Communication, October 2021.

11: European Commission, ‘Identifying Europe’s recovery needs’, Staff working document, May 2020.

12: From European Commission, ‘Climate target plan impact assessment’, 2020, and McKinsey, ‘Net zero Europe report’, 2020.

13: See for a broader discussion Carbon Brief, ‘Why cement emissions matter for climate change’, September 2018. The figures here are taken from Agora Energiewende and Wuppertal Institute, ‘Breakthrough strategies for climate-neutral industry in Europe: Policy and technology pathways for raising EU climate ambition’, 2021.

14: European Commission, ‘Climate Target Plan impact assessment’, 2020; McKinsey, ‘Net Zero Europe’, 2020.

15: The rail and public transport infrastructure investment needs are from the European Commission’s staff working paper accompanying the proposal for the Next Generation EU (SWD (2020) 456 final), expressed in 2020 prices.

16: European Commission, ‘Climate Target Plan impact assessment’, 2020.

17: McKinsey, ‘Net Zero Europe’, 2020.

18: Sam Lowe, ‘The EU’s carbon border adjustment mechanism – How to make it work for developing countries’, CER policy brief, April 2021.

19: The figure is close to the estimate of Garicano (‘Combining environmental and fiscal sustainability’, 2022), who estimated the annual public spending gap at €160 billion. Our estimate includes subsidies to investment to make consumption of materials more efficient (circular economy), as well as the compensation to low-income households for higher heating and power costs. See also Claudio Baccianti and Janek Steitz, ‘How to align the EU fiscal framework with the Green Deal’, Agora Energiewende Blog, February 2022.

20: The Connecting Europe Facility has co-financed large-scale trans-European energy infrastructure projects, providing € 4.6 billion of grants between 2014 and 2020.

21: European Commission, ‘Tackling rising energy prices: a toolbox for action and support’, Communication, October 2021.

22: European Commission, ‘Annex to the report on the state of the Energy Union - Contribution to the European Green Deal and the Union’s recovery’, October 2021.

23: European Commission, ‘Annex to the report on the state of the Energy Union - Contribution to the European Green Deal and the Union’s recovery’, October 2021.

24: IMF, ‘Article IV consultation staff documents’, June 2021, and European Commission, ‘Recommendation for Council recommendation delivering a Council opinion on the 2021 Stability Programme of Italy’, June 2021.

25: Elisabetta Cornago and John Springford, ‘Why the EU’s recovery fund should be made permanent’, CER Policy Brief, November 2021; Zsolt Darvas and Guntram Wolff, ‘A green fiscal pact: climate investment in times of budget consolidation’, Bruegel, September 2021.

Claudio Baccianti is Project Manager EU Sustainable Finance, Agora Energiewende and Christian Odendahl European economics editor at The Economist and former chief economist of the CER

May 2022

This work is being supported by a grant from the European Climate Foundation.

View press release

Download full publication